Accounting Basics(Explanation)

More ways to study this topic:

Explanation

1.

Part 1Part 1

2.

Part 2

3.

Part 3

4.

Part 4

5.

Part 5

6.

Part 6

7.

Part 7

Introduction to

Accounting Basics

This explanation of accounting

basics will introduce you to some basic accounting principles, accounting

concepts, and accounting terminology. Once you become familiar with some of

these terms and concepts, you will feel comfortable navigating through the

explanations, quizzes, puzzles, and other features of AccountingCoach.com.

Some of the basic accounting

terms that you will learn include revenues, expenses, assets, liabilities,

income statement, balance sheet, and statement of cash flows. You will become

familiar with accounting debits and credits as we show you how to record

transactions. You will also see why two basic accounting principles, the

revenue recognition principle and the matching principle, assure that a

company's income statement reports a company's profitability.

In this explanation of accounting

basics, and throughout all of the free materials and the PRO materials—we will

often omit some accounting details and complexities in order to present clear

and concise explanations. This means that you should always seek professional

advice for your specific circumstances.

Note: We provide visual

tutorials, flashcards, exam questions, videos, and forms for members ofAccountingCoach PRO.

A Story for

Relating to Accounting Basics

We will present the basics of

accounting through a story of a person starting a new business. The person is

Joe Perez—a savvy man who sees the need for a parcel delivery service in his

community. Joe has researched his idea and has prepared a business plan that

documents the viability of his new business.

Joe has also met with an attorney

to discuss the form of business he should use. Given his specific situation,

they concluded that a corporation will be best. Joe decides that the name for

his corporation will be Direct Delivery, Inc. The attorney also advises Joe on

the various permits and government identification numbers that will be needed

for the new corporation.

Joe is a hard worker and a smart

man, but admits he is not comfortable with matters of accounting. He assumes he

will use some accounting software, but wants to meet with a professional

accountant before making his selection. He asks his banker to recommend a

professional accountant who is also skilled in explaining accounting to someone

without an accounting background. Joe wants to understand the financial

statements and wants to keep on top of his new business. His banker recommends

Marilyn, an accountant who has helped many of the bank's small business

customers.

At his first meeting with

Marilyn, Joe asks her for an overview of accounting, financial statements, and

the need for accounting software. Based on Joe's business plan, Marilyn sees

that there will likely be thousands of transactions each year. She states that

accounting software will allow for the electronic recording, storing, and

retrieval of those many transactions. Accounting software will permit Joe to

generate the financial statements and other reports that he will need for

running his business.

Joe seems puzzled by the term

transaction, so Marilyn gives him five examples of transactions that Direct

Delivery, Inc. will need to record:

1. Joe will no

doubt start his business by putting some of his own personal money into it. In

effect, he is buying shares of Direct Delivery's common stock.

2. Direct Delivery

will need to buy a sturdy, dependable delivery vehicle.

3. The business

will begin earning fees and billing clients for delivering their parcels.

4. The business

will be collecting the fees that were earned.

5. The business

will incur expenses in operating the business, such as a salary for Joe,

expenses associated with the delivery vehicle, advertising, etc.

With thousands of such

transactions in a given year, Joe is smart to start using accounting software

right from the beginning. Accounting software will generate sales invoices and

accounting entries simultaneously, prepare statements for customers with no

additional work, write checks, automatically update accounting records, etc.

By getting into the habit of

entering all of the day's business transactions into his computer, Joe will be

rewarded with fast and easy access to the specific information he will need to

make sound business decisions. Marilyn tells Joe that accounting's

"transaction approach" is useful, reliable, and informative. She has

worked with other small business owners who think it is enough to simply

"know" their company made $30,000 during the year (based only on the

fact that it owns $30,000 more than it did on January 1). Those are the people

who start off on the wrong foot and end up in Marilyn's office looking for

financial advice.

If Joe enters all of Direct

Delivery's transactions into his computer, good accounting software will allow

Joe to print out his financial statements with a click of a button. In Parts 2

through 7 Marilyn will explain the content and purpose of the three main

financial statements:

1. Income

Statement

2. Balance Sheet

3. Statement of

Cash Flows

Income Statement

Marilyn points out that an income statement

will show how profitable Direct Delivery has

been during the time interval shown in the statement's heading. This period of

time might be a week, a month, three months, five weeks, or a year—Joe can

choose whatever time period he deems most useful.

The reporting of profitability involves two

things: the amount that was earned (revenues) andthe expenses necessary to earn

the revenues. As you will see next, the term revenues is not the same as receipts, and the term expenses involves more than just writing a check to pay

a bill.

A. Revenues

The main revenues for

Direct Delivery are the fees it earns for delivering parcels. Under theaccrual basis of accounting (as opposed to the less-preferred cash method of accounting), revenues are recorded when they are earned, not when the company receives the money. Recording revenues when they are

earned is the result of one of the basic accounting principles known as the revenue recognition principle.

For example, if Joe

delivers 1,000 parcels in December for $4 per delivery, he has technicallyearned fees totalling $4,000 for that month. He sends

invoices to his clients for these fees and his terms require that his clients

must pay by January 10. Even though his clients won't be paying Direct Delivery

until January 10, the accrual basis of accounting requires that the $4,000 be

recorded as December revenues, since that

is when the delivery work actually took place. After expenses are matched with

these revenues, the income statement for December will show just how profitable the company was in delivering parcels in

December.

When Joe receives the

$4,000 worth of payment checks from his customers on January 10, he will make

an accounting entry to show the money was received. This $4,000 of receipts

will not be considered to be January revenues, since the revenues were already reported as revenues in December

when they were earned. This $4,000 of receipts will be recorded in January as a

reduction in Accounts

Receivable. (In December Joe had made an entry to Accounts Receivable and

to Sales.)

B. Expenses

Now Marilyn turns to

the second part of the income statement—expenses. The December income statement

should show expenses incurred during December

regardless of when the company actually paid for the expenses. For example, if Joe hires

someone to help him with December deliveries and Joe agrees to pay him $500 on

January 3, that $500 expense needs to be shown on the December income statement. The actual date that the

$500 is paid out doesn't matter. What matters is when the work was done—when

the expense was incurred—and in this case, the

work was done in December. The $500 expense is counted as a December expense

even though the money will not be paid out until January 3. The recording of

expenses with the related revenues is associated with another basic accounting

principle known as thematching principle.

Marilyn explains to

Joe that showing the $500 of wages expense on the December income statement

will result in a matching of the cost of the

labor used to deliver the December parcels with the revenues from delivering

the December parcels. This matching principle is very important in measuring

just how profitable a company was during a given time period.

Marilyn is delighted

to see that Joe already has an intuitive grasp of this basic accounting

principle. In order to earn revenues in December, the company had to incur some

business expenses in December, even if the expenses won't be paid until January. Other expenses to be matched

with December's revenues would be such things as gas for the delivery van and

advertising spots on the radio.

Joe asks Marilyn to

provide another example of a cost that wouldn't be paid in December, but would

have to be shown/matched as an expense on December's income statement. Marilyn

uses the Interest Expense on borrowed money as an example. She asks Joe

to assume that on December 1 Direct Delivery borrows $20,000 from Joe's aunt

and the company agrees to pay his aunt 6% per year in interest, or $1,200 per

year. This interest is to be paid in a lump sum each on December 1 of each

year.

Now even though the

interest is being paid out to his aunt only once per year as a lump sum, Joe

can see that in reality, a little bit of that interest expense is incurred each and every day he's in business. If Joe is

preparing monthly income statements, Joe

should report one month of Interest Expense on each month's income statement.

The amount that Direct Delivery will incur as Interest Expense will be $100 per

month all year long ($20,000 x 6% ÷ 12). In other words, Joe needs to match

$100 of interest expense with each month's revenues. The interest expense is

considered a cost that is necessary to earn the revenues shown on the income

statements.

Marilyn explains to

Joe that the income statement is a bit more complicated than what she just

explained, but for now she just wants Joe to learn some basic accounting

concepts and some of the accounting terminology. Marilyn does make sure,

however, that Joe understands one simple yet important point: an income statement, does not report the cash coming in—rather, its purpose is to

(1) report the revenues earned by the company's efforts during the period,

and

(2) report the expenses incurred by the company during the same period.

The purpose of the

income statement is to show a company's profitability during a specific period of time. The

difference (or "net") between the revenues and expenses for Direct

Delivery is often referred to as the bottom line and it is labeled as either Net Income or Net Loss.

Balance

Sheet - Assets

Marilyn moves on to explain the balance sheet,

a financial statement that reports the amount of a company's (A) assets, (B) liabilities, and (C) stockholders' (or owner's) equity at a

specificpoint in time.

Because the balance sheet reflects a specific point in time rather than a period of time, Marilyn likes to refer to the balance sheet

as a "snapshot" of a company's financial position at a given moment.

For example, if a balance sheet is dated December 31, the amounts shown on the

balance sheet are the balances in the accounts after all transactions

pertaining to December 31 have been recorded.

(A) Assets

Assets are things that a company owns and are

sometimes referred to as the resources of the company. Joe readily understands

this—off the top of his head he names things such as the company's vehicle, its

cash in the bank, all of the supplies he has on hand, and the dolly he uses to

help move the heavier parcels. Marilyn nods and shows Joe how these are

reported in accounts called Vehicles, Cash, Supplies, and Equipment. She mentions one asset Joe hadn't considered—Accounts

Receivable. If Joe delivers parcels, but isn't paid immediately for the

delivery, the amount owed to Direct Delivery is an asset known as Accounts

Receivable.

Prepaids

Marilyn brings up another less obvious

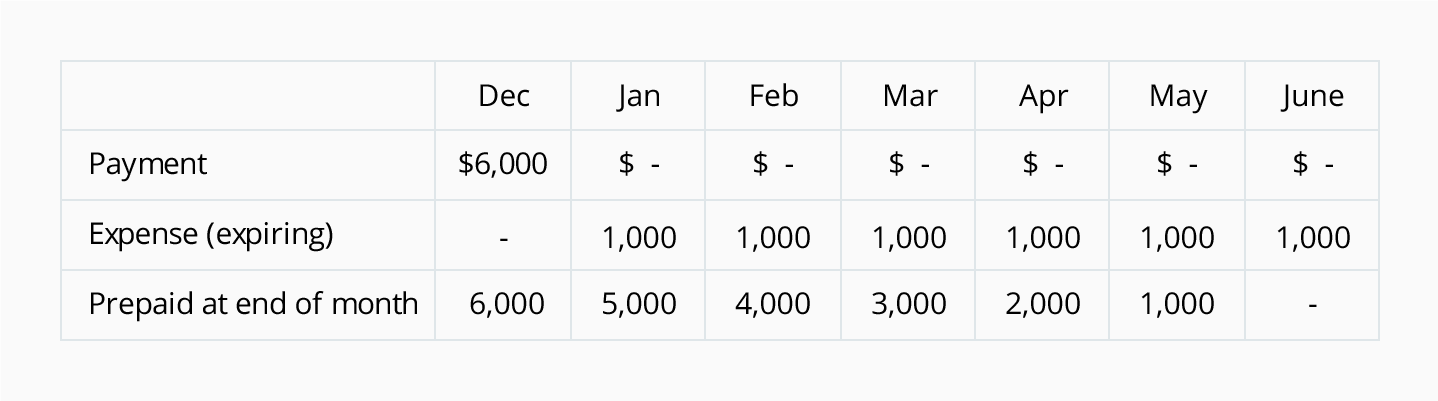

asset—the unexpired portion of prepaid expenses.Suppose Direct Delivery pays $1,200 on

December 1 for a six-month insurance premium on its delivery vehicle. That

divides out to be $200 per month ($1,200 ÷ 6 months). Between December 1 and

December 31, $200 worth of insurance premium is "used up" or

"expires". Theexpired amount will be

reported as Insurance Expense on December's income statement. Joe asks

Marilyn where the remaining $1,000 of unexpired insurance premium would be

reported. On the December 31 balance sheet, Marilyn tells him, in an asset

account calledPrepaid Insurance.

Other examples of things that might be paid for before they are

used include supplies and annual dues to a trade association. The portion that

expires in the current accounting period is listed as an expense on the income

statement; the part that has not yet expired is listed as an asset on the

balance sheet.

Marilyn assures Joe that he will soon see a significant link

between the income statement and balance sheet, but for now she continues with

her explanation of assets.

Cost Principle and Conservatism

Joe learns that each of his company's assets

was recorded at its original cost,

and even if the fair market value of an item increases, an accountant will not

increase the recorded amount of that asset on the balance sheet. This is the

result of another basic accounting principle known as the cost principle.

Although accountants generally do not increase the value of an asset, they might decrease its value as a result of a concept known as conservatism. For example, after a few months in business,

Joe may decide that he can help out some customers—as well as earn additional

revenues—by carrying an inventory of packing boxes to sell. Let's say that

Direct Delivery purchased 100 boxes wholesale for $1.00 each. Since the time

when Joe bought them, however, the wholesale price of boxes has been cut by 40%

and at today's price he could purchase them for $0.60 each. Because the

replacement cost of his inventory ($60) is less than the original recorded cost ($100), the principle of conservatism

directs the accountant to report the lower amount ($60) as the asset's value on

the balance sheet.

In short, the cost principle generally prevents assets from

being reported at more than cost, while conservatism might require assets to be

reported at less than their cost.

Depreciation

Joe also needs to know that the reported

amounts on his balance sheet for assets such as equipment, vehicles, and

buildings are routinely reduced by depreciation. Depreciation is required by

the basic accounting principle known as the matching principle. Depreciation is used for assets whose life is

not indefinite—equipment wears out, vehicles become too old and costly to

maintain, buildings age, and some assets (like computers) become obsolete.

Depreciation is the allocation of the cost of the asset to Depreciation Expense on the income statement over its useful life.

As an example, assume that Direct Delivery's

van has a useful life of five years and was purchased at a cost of $20,000. The

accountant might match $4,000 ($20,000 ÷ 5 years) of Depreciation Expense with

each year's revenues for five years. Each year the carrying amountof the van will be reduced by $4,000. (The carrying amount—or

"book value"—is reported on the balance sheet and it is the cost of

the van minus the total depreciation since the van was acquired.) This means

that after one year the balance sheet will report the carrying amount of the

delivery van as $16,000, after two years the carrying amount will be $12,000,

etc. After five years—the end of the van's expected useful life—its carrying

amount is zero.

Joe wants to be certain that he understands

what Marilyn is telling him regarding the assets on the balance sheet, so he

asks Marilyn if the balance sheet is, in effect, showing what the company's

assets are worth. He is surprised to hear Marilyn say that the assets are not reported on the balance sheet at their worth

(fair market value). Long-term assets (such as buildings, equipment, and

furnishings) are reported at their cost minus the amounts already sent to the income

statement as Depreciation Expense. The result is that a building's market value

may actually have increased since it was acquired, but the amount on the

balance sheet has beenconsistently reduced as the accountant moved some of its cost to Depreciation Expense

on the income statement in order to achieve the matching principle.

Another asset, Office Equipment, may have a fair market value that is much

smaller than the carrying amount reported on the balance sheet. (Accountants

view depreciation as an allocationprocess—allocating

the cost to expense in order to match the costs with the revenues generated by

the asset. Accountants do not consider depreciation

to be a valuation process.) The asset Land is not depreciated, so it will appear at its

original cost even if the land is now worth one hundred times more than its

cost.

Short-term (current) asset amounts are likely to be close to

their market values, since they tend to "turn over" in relatively

short periods of time.

Marilyn cautions Joe that the balance sheet reports only the

assets acquired and only at the cost reported in the transaction. This means

that a company's reputation—as excellent as it might be—will not be listed as

an asset. It also means that Jeff Bezos will not appear as an asset on

Amazon.com's balance sheet; Nike's logo will not appear as an asset on its

balance sheet; etc. Joe is surprised to hear this, since in his opinion these

items are perhaps the most valuable things those companies have. Marilyn tells

Joe that he has just learned an important lesson that he should remember when

reading a balance sheet.

Balance

Sheet - Liabilities and Stockholders' Equity

(B) Liabilities

The balance sheet reports Direct Delivery's liabilities as of the date noted in the heading of the

balance sheet. Liabilities are obligations of the company; they are amounts

owed to others as of the balance sheet date. Marilyn gives Joe some examples of

liabilities: the loan he received from his aunt (Notes Payable or Loan Payable), the interest on the loan he owes to his aunt(Interest Payable), the amount he owes to the supply store for items purchased on

credit (Accounts

Payable),

the wages he owes an employee but hasn't yet paid to him(Wages Payable).

Another liability is money received in advance

of actually earning the money. For

example, suppose that Direct Delivery enters into an agreement with one of its

customers stipulating that the customer prepays $600 in return for the delivery

of 30 parcels every month for 6 months. Assume Direct Delivery receives that

$600 payment on December 1 for deliveries to be made between December 1 and May

31. Direct Delivery has a cash receipt of $600 on December 1,

but it does not have revenues of $600

at this point. It will have revenues only when it earns them by delivering the parcels. On December 1,

Direct Delivery will show that its asset Cashincreased by $600, but it will also have to

show that it has a liability of $600. (It has the liability to deliver $600 of parcels within 6 months, or

return the money.)

The liability account involved in the $600

received on December 1 is Unearned Revenue. Each month, as the 30 parcels are delivered,

Direct Delivery will be earning $100, and as a result, each month $100 moves

from the account Unearned Revenue to Service Revenues. Each month Direct Delivery's liability

decreases by $100 as it fulfills the agreement by delivering parcels and each

month its revenues on the income statement increase by $100.

(C) Stockholders' Equity

If the company is a corporation, the third section of a

corporation's balance sheet is Stockholders' Equity. (If the company is a sole

proprietorship, it is referred to as Owner's Equity.) The amount of

Stockholders' Equity is exactly the difference between the asset amounts and

the liability amounts. As a result accountants often refer to Stockholders'

Equity as the difference (or residual) of assets minus liabilities. Stockholders'

Equity is also the "book value" of the corporation.

Since the corporation's assets are shown at

cost or lower (and not at their market values) it is important that you do not associate the reported amount of Stockholders'

Equity with the market value of the corporation. (Hence, it is a poor choice of

words to refer to Stockholders' Equity as the corporation's "net

worth".) To find the market value of a corporation, you should obtain the

services of a professional familiar with valuing businesses.

Within the Stockholders' Equity section you

may see accounts such as Common Stock,Paid-in Capital in Excess of Par Value-Common Stock, Preferred Stock, Retained Earnings, andCurrent Year's Net Income.

The account Common Stock will be increased

when the corporation issues shares of stock in exchange for cash (or some other

asset). Another account Retained Earnings will increase when the corporation

earns a profit. There will be a decrease when the corporation has a net loss.

This means that revenues will automatically cause an increase in Stockholders' Equity and expenses will

automatically cause a decrease in Stockholders'

Equity. This illustrates a link between a company's balance sheet and income

statement.

Statement of Cash Flows

The

third financial statement that Joe needs to understand is the Statement of Cash

Flows. This statement shows how Direct Delivery's cash amount has changed

during the time interval shown in the heading of the statement. Joe will be

able to see at a glance the cash generated and used by his company's operating

activities, its investing activities, and its financing activities. Much of the

information on this financial statement will come from Direct Delivery's

balance sheets and income statements.

Note: To learn more about the statement of cash flows,

visit:Explanation of Cash Flow Statement Quiz for Cash Flow Statement

The

three financial reports that Marilyn introduced to Joe—the income statement,

the balance sheet, and the statement of cash flows—represent one segment of the

valuable output that good accounting software can generate for business owners.

Marilyn

now explains to Joe the basics of getting started with recording his

transactions.

Double Entry System

The field of

accounting—both the older manual systems and today's basic accounting

software—is based on the 500-year-old accounting procedure known as double entry.

Double entry is a simple yet powerful concept: each and every one of a

company's transactions will result in an amount recorded into at least two of the accounts in the accounting

system.

The

Chart of Accounts

To begin the process of

setting up Joe's accounting system, he will need to make a detailed listing of

all the names of the accounts that Direct Delivery, Inc. might find useful for

reporting transactions. This detailed listing is referred to as a chart of accounts.

(Accounting software often provides sample charts of accounts for various types

of businesses.)

As

he enters his transactions, Joe will find that the chart of accounts will help

him select the two (or more) accounts that are involved. Once Joe's business

begins, he may find that he needs to add more account names to the chart of

accounts, or delete account names that are never used. Joe can tailor his chart

of accounts so that it best sorts and reports the transactions of his business.

Because

of the double entry system all of Direct Delivery's transactions will involve a

combination of two or more accounts from the balance sheet and/or the income

statement. Marilyn lists out some sample accounts that Joe will probably need

to include on his chart of accounts:

Note: To learn more about the chart of accounts, visit:Explanation of Chart of Accounts Quiz for Chart of Accounts

Balance

Sheet accounts:

- Asset accounts (Examples: Cash, Accounts Receivable, Supplies, Equipment)

- Liability accounts (Examples: Notes Payable, Accounts Payable, Wages Payable)

- Stockholders' Equity accounts (Examples: Common Stock, Retained Earnings)

Income

Statement accounts:

- Revenue accounts (Examples: Service Revenues, Investment Revenues)

- Expense accounts (Examples: Wages Expense, Rent Expense, Depreciation Expense)

To

help Joe really understand how this works, Marilyn illustrates the double entry

with some sample transactions that Joe will likely encounter.

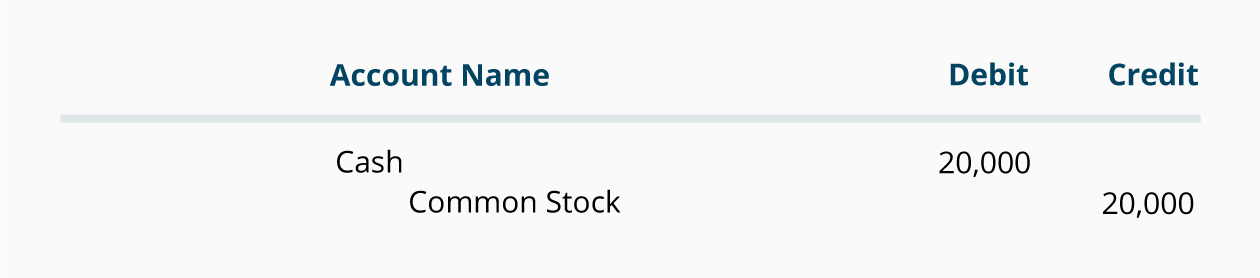

Sample Transaction #1

On December 1, 2014 Joe

starts his business Direct Delivery, Inc. The first transaction that Joe will

record for his company is his personal investment of $20,000 in exchange for

5,000 shares of Direct Delivery's common stock. Direct Delivery's accounting

system will show an increase in its account Cash from zero to $20,000, and an

increase in its stockholders' equity account Common Stock by $20,000. Both of

these accounts are balance sheet accounts. There are no revenues because no delivery fees were earned by the company, and there were no

expenses.

After

Joe enters this transaction, Direct Delivery's balance sheet will look like

this:

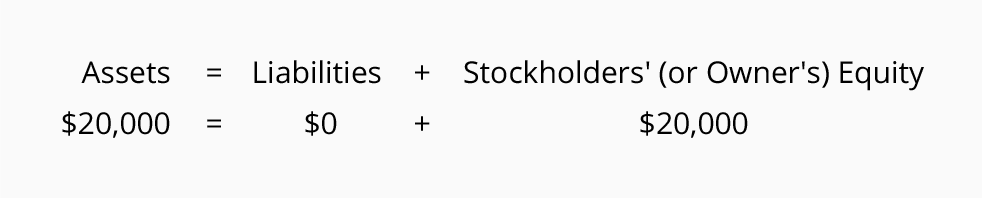

Marilyn asks Joe if he can

see that the balance sheet is just that-in

balance. Joe looks at the total of $20,000 on the asset side, and looks

at the $20,000 on the right side, and says yes, of course, he can see that it

is indeed in balance.

Marilyn shows Joe something

called the basic accounting equation, which, she explains, is

really the same concept as the balance sheet, it's just presented in an

equation format:

The

accounting equation (and the balance sheet) should always be in balance.

Debits

and Credits

Did

the first sample transaction follow the double entry system and affect two or

more accounts? Joe looks at the balance sheet again and answers yes, both Cash

and Common Stock were affected by the transaction.

Marilyn introduces the next

basic accounting concept: the double entry system requires that the same dollar

amount of the transaction must be entered on both the left side of one account, and on the right side of another account. Instead of the

word left, accountants use the word debit;

and instead of the word right, accountants use the word credit.

(The terms debit and credit are derived from Latin terms used 500

years ago.)

Here's a Tip

Debit means left.

Credit means right.

Joe

asks Marilyn how he will know which accounts he should debit—meaning he should

enter the numbers on the left side of one account—and which accounts he should

credit—meaning he should enter the numbers on the right side of another

account. Marilyn points back to the basic accounting equation and tells Joe

that if he memorizes this simple equation, it will be easier to understand the

debits and credits.

Here's a Tip

Memorizing

the simple accounting equation will help you learn the debit and credit rules

for entering amounts into the accounting records.

Let's

take a look at the accounting equation again:

Just as assets are on the

left side (or debit side) of the accounting equation, the asset accounts in the

general ledger have their balances on the left side. To increase an asset account's balance, you put

more on the left side of the asset account. In accounting jargon, you debit the asset account.

To decrease an

asset account balance you credit the

account, that is, you enter the amount on the right side.

Just as liabilities and

stockholders' equity are on the right side (or credit side) of the accounting

equation, the liability and equity accounts in the general ledger have their

balances on the right side. To increase the

balance in a liability or stockholders' equity account, you put more on the

right side of the account. In accounting jargon, you credit the liability or

the equity account. Todecrease a liability or equity, you debit the

account, that is, you enter the amount on the left side of the account.

As

with all rules, there are exceptions, but Marilyn's reference to the accounting

equation may help you to learn whether an account should be debited or

credited.

Since many transactions

involve cash, Marilyn suggests that Joe memorize how the Cash account is

affected when a transaction involves cash: if Direct Delivery receives cash, the Cash account is debited; when

Direct Delivery pays cash,

the Cash account is credited.

Here's a Tip

When

a company receives cash,

the Cash account is debited.

When

the company pays cash,

the Cash account is credited.

Marilyn refers to the

example of December 1. Since Direct Delivery received $20,000 in cashfrom

Joe in exchange for 5,000 shares of common stock, one of the accounts for this

transaction is Cash. Since cash was received, the Cash account will be debited.

In keeping with double

entry, two (or more) accounts need to be involved. Because the first account

(Cash) was debited, the second account needs to be credited.

All Joe needs to do is find the right account to credit. In this case, the

second account is Common Stock. Common stock is part of stockholders' equity,

which is on the right side of the accounting equation. As a result, it should

have a credit balance, and to increase its balance the account needs to becredited.

Accountants

indicate accounts and amounts using the following format:

Accountants

usually first show the account and amount to be debited. On the next line, the

account to be credited is indented and the amount appears further to the right

than the debit amount shown in the line above. This entry format is referred to

as a general journal entry.

(With

the decrease in the price of computers and accounting software, it is rare to

find a small business still using a manual system and making entries by hand.

Accounting software has made the process of recording transactions so much

easier that the general journal is rarely needed. In fact, entries are often

generated automatically when a check or sales invoice is prepared.)

Sample Transactions #2 - #3

Sample

Transaction #2

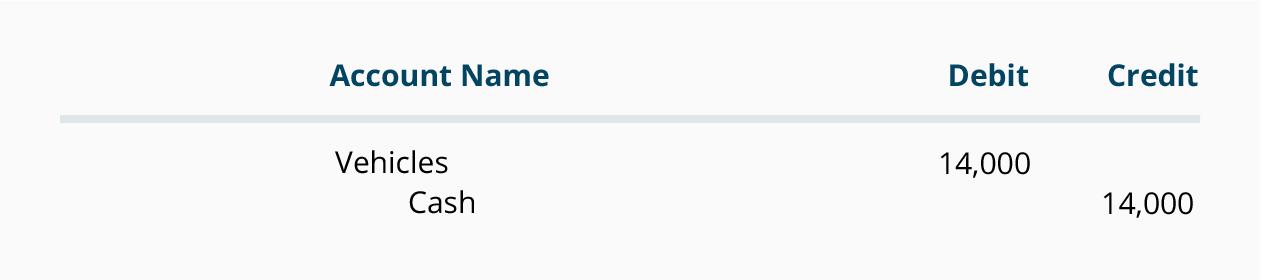

Marilyn illustrates for Joe

a second transaction. On December 2, Direct Delivery purchases a used delivery

van for $14,000 by writing a check for $14,000. The two accounts involved are

Cash and Vehicles (or Delivery Equipment).

When the check is written, the accounting software will automatically make the

entry into these two accounts.

Marilyn explains to Joe

what is happening within the software. Since the company pays $14,000, the Cash account is credited.

(Accountants consider the checking account to be Cash, and the TIP you

learned is that when cash is paid, you credit Cash.)

So we know that the Cash account will be credited for $14,000 and we know the other

account will have to be debited for

$14,000. We need only identify the best account to debit. In this case we

choose Vehicles (or Delivery Equipment) and the entry is:

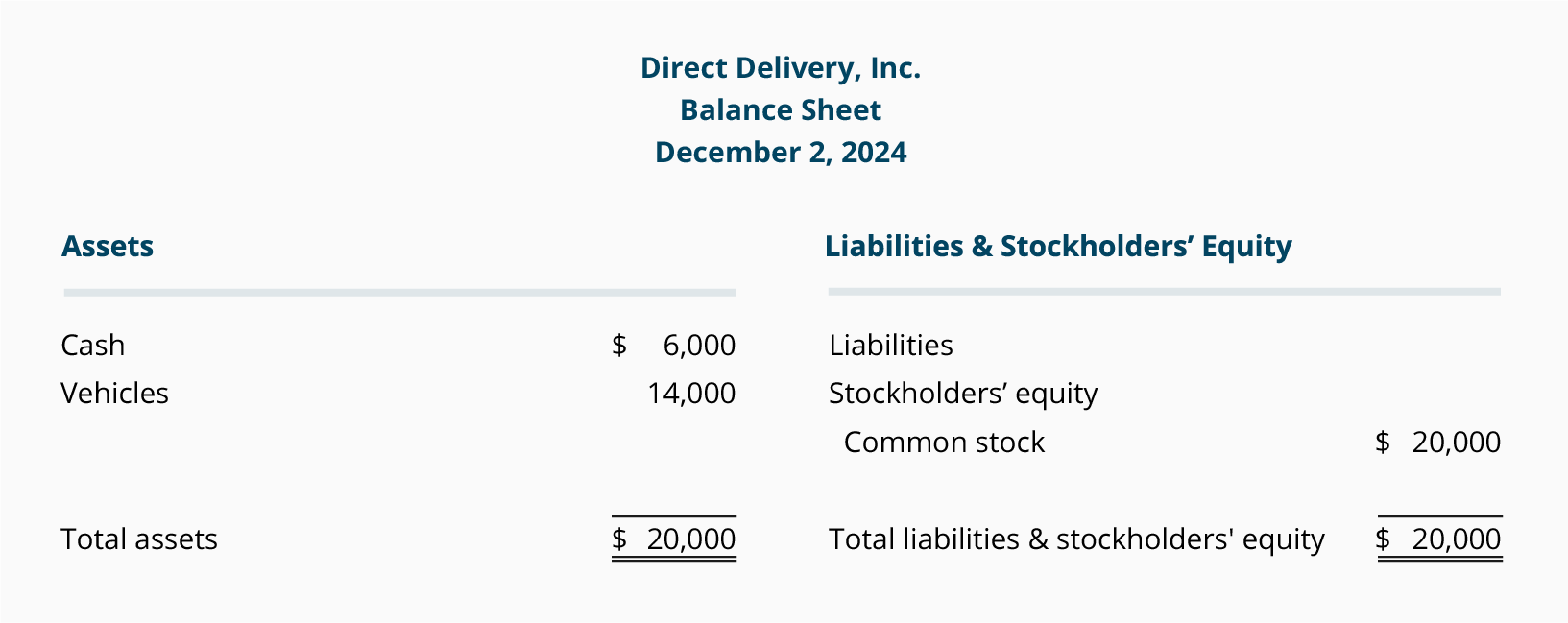

The

balance sheet will look like this after the vehicle transaction is recorded:

The

balance sheet and the accounting equation remain in balance:

As

you can see in the balance sheet, the asset Cash decreased by $14,000 and

another asset Vehicles increased by $14,000. Liabilities and stockholders'

equity were not involved and did not change.

Sample

Transaction #3

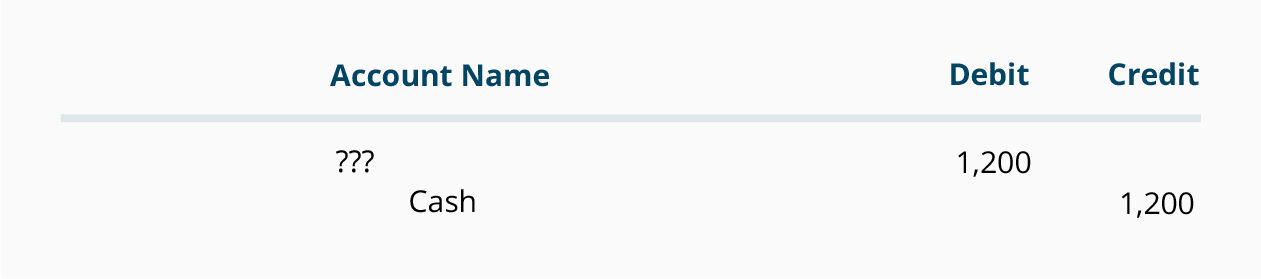

The

third sample transaction also occurs on December 2 when Joe contacts an

insurance agent regarding insurance coverage for the vehicle Direct Delivery

just purchased. The agent informs him that $1,200 will provide insurance

protection for the next six months. Joe immediately writes a check for $1,200

and mails it in.

Let's consider this transaction.

Using double entry, we know there must be a minimum of two accounts

involved—one (or more) of the accounts must be debited,

and one (or more) must becredited.

Since a check is written,

we know that one of the accounts involved is Cash. Since cash waspaid, the Cash account will be credited.

(Take another look at the last TIP.) While we have not yet identified the second account, what we

do know for certain is that the second account will have to be debited.

At this point we have most

of the entry-all we are missing is the name of

the account to be debited:

We

know the transaction involves insurance, and a quick look through the chart of

accounts reveals two possibilities:

Prepaid Insurance (an asset account reported on the balance sheet) andInsurance Expense (an expense account reported on the income statement)

Assets

include costs that are not yet expired (not yet used up), while expenses are

costs that have expired (have been used up). Since the $1,200 payment is for an

expense that will not expire in its entirety within the current month, it would

be logical to debit the account Prepaid Insurance. (At the end of each month,

when $200 has expired, $200 will be moved from Prepaid Insurance to Insurance

Expense.)

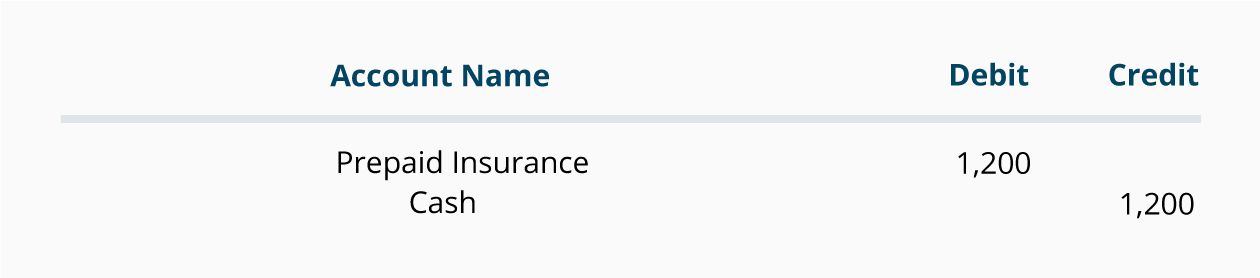

The

entry in the general journal format is:

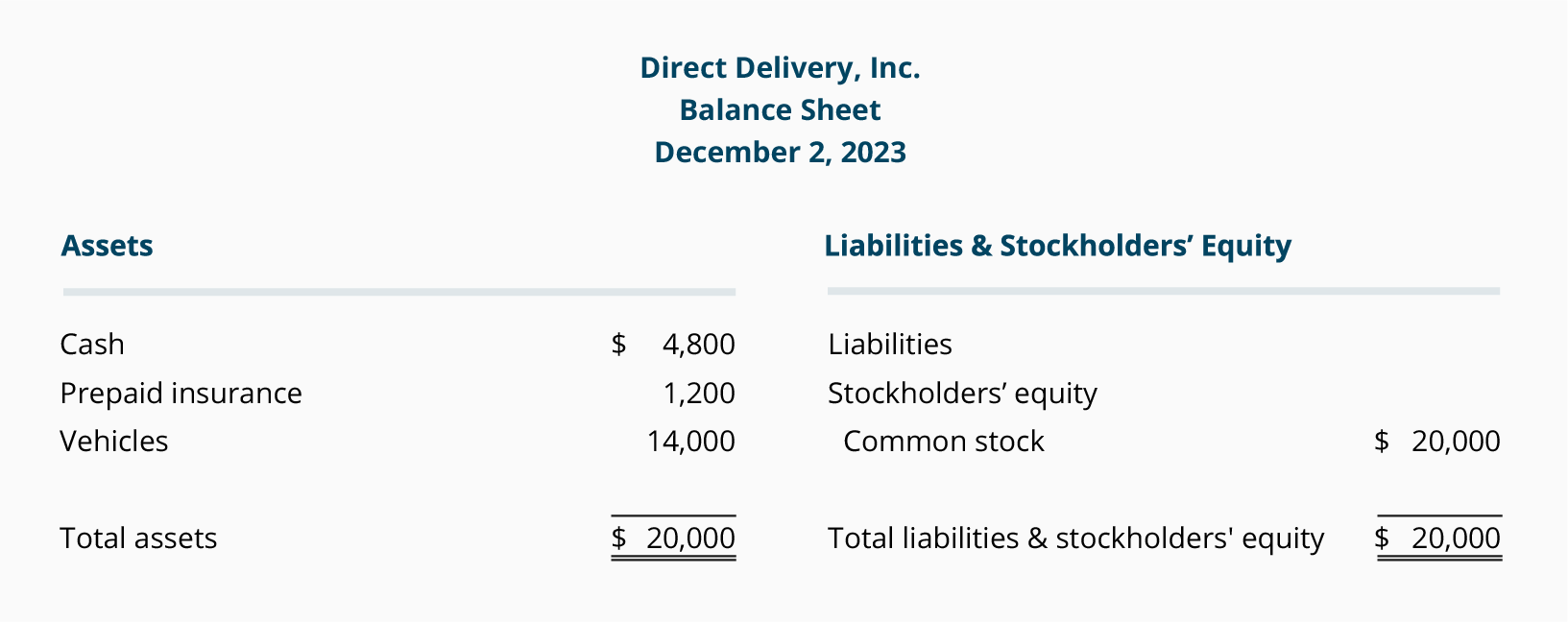

After

the first three transactions have been recorded, the balance sheet will look

like this:

Again,

the balance sheet and the accounting equation are in balance and all of the

changes occurred on the asset/left/debit side of the accounting equation.

Liabilities and Stockholders' Equity were not affected by the insurance

transaction.

Sample Transactions #4 - #6

Sample

Transaction #4

The

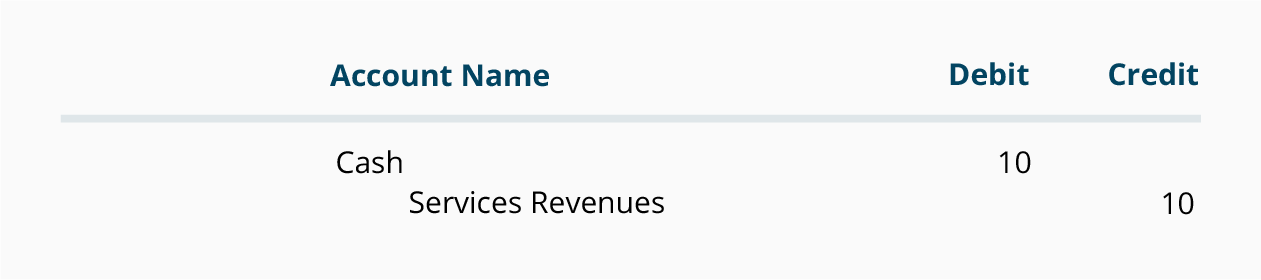

fourth transaction occurs on December 3, when a customer gives Direct Delivery

a check for $10 to deliver two parcels on that day. Because of double entry, we

know there must be a minimum of two accounts involved—one of the accounts must

be debited, and one of the accounts must be credited.

Because Direct Delivery received $10, it must debit the account Cash. It must also credit a second account for $10. The second

account will be Service Revenues, an income statement account. The reason

Service Revenues is credited is

because Direct Delivery must report that itearned $10 (not because it received $10).

Recording revenues when they are earned results from a basic accounting

principle known as the revenue recognition principle. The following tip

reflects that principle.

Here's a Tip

Revenues

accounts are credited when

the company earns a

fee (or sells merchandise) regardless of whether cash is received at the time.

Here

are the two parts of the transaction as they would look in the general journal

format:

Sample

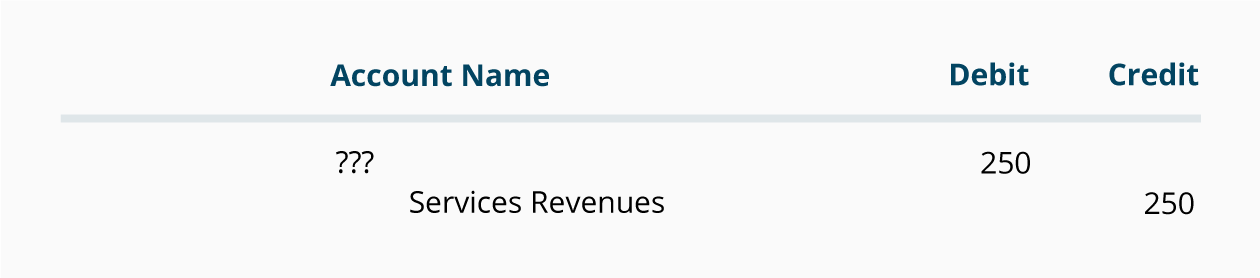

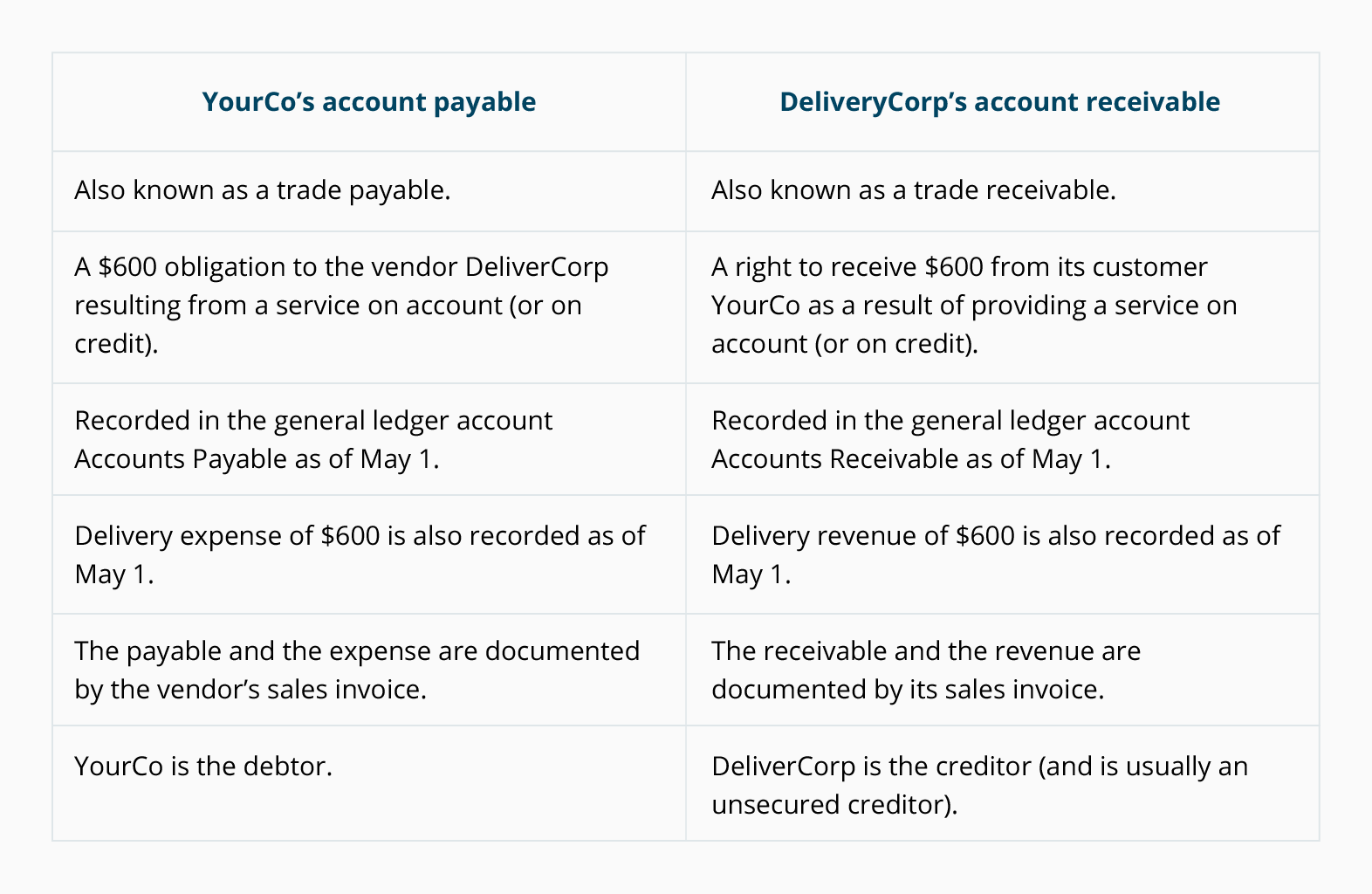

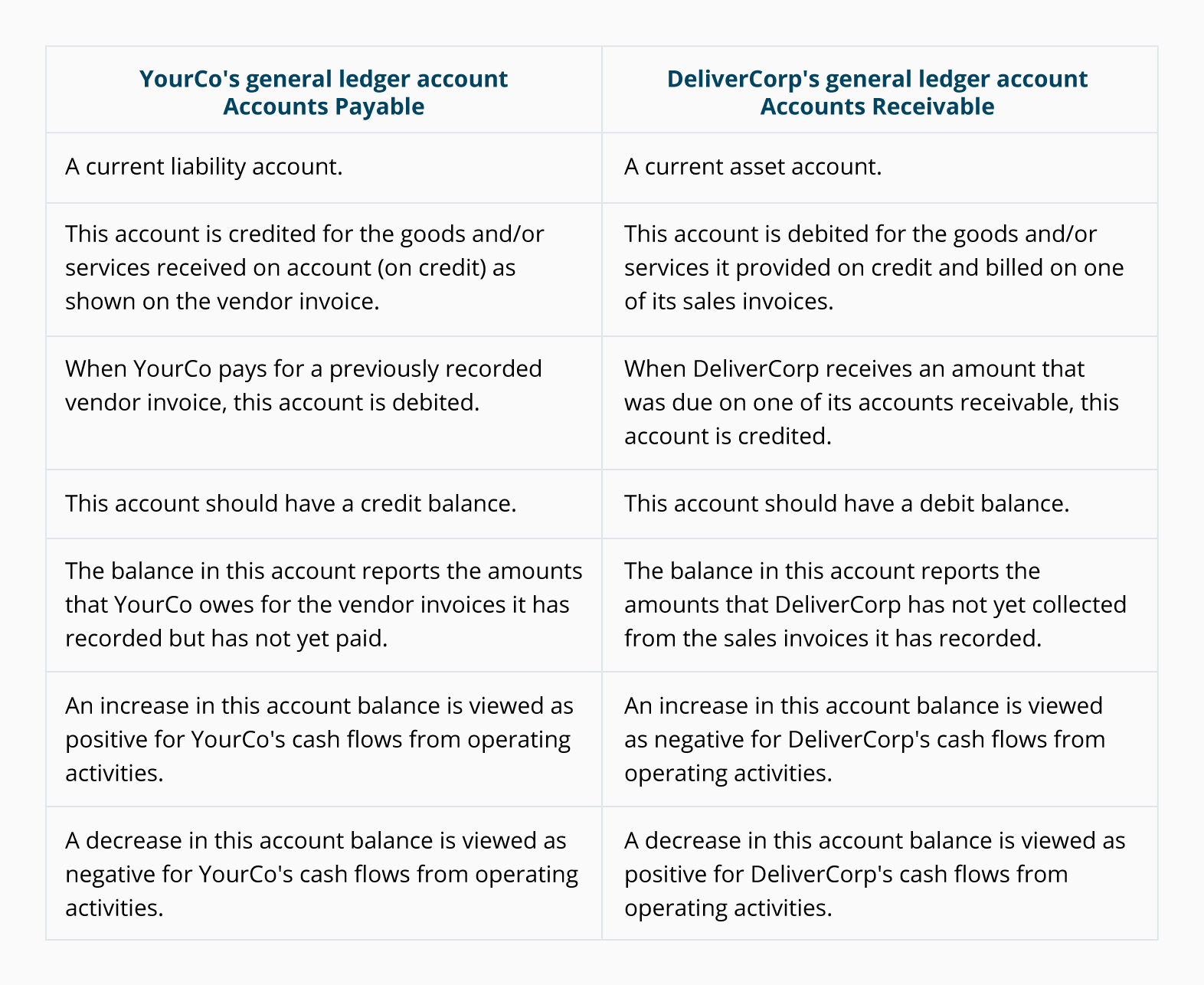

Transaction #5

Let's

assume that on December 3 the company gets its second customer-a local company

that needs to have 50 parcels delivered immediately. Joe's price of $250 is

very appealing, so Joe's company is hired to deliver the parcels. The customer

tells Joe to submit an invoice for the $250, and they will pay it within seven

days.

Joe delivers the 50 parcels

on December 3 as agreed, meaning that on December 3 Direct Delivery has earned $250. Hence the $250 is reported as

revenues on December 3, even though the company did not

receive any cash on that day. The effort needed

to complete the job was done on December 3. (Depositing the check for $250 in

the bank when it arrives seven days later is not considered to take any

effort.)

Let's

identify the two accounts involved and determine which needs a debit and which

needs a credit.

Because Direct Delivery has

earned the fees, one account will be a revenues account, such as Service

Revenues. (If you refer back to the last TIP, you

will read that revenue accounts—such as Service Revenues—are usually credited,

meaning the second account will need to be debited.)

In

the general journal format, here's what we have identified so far:

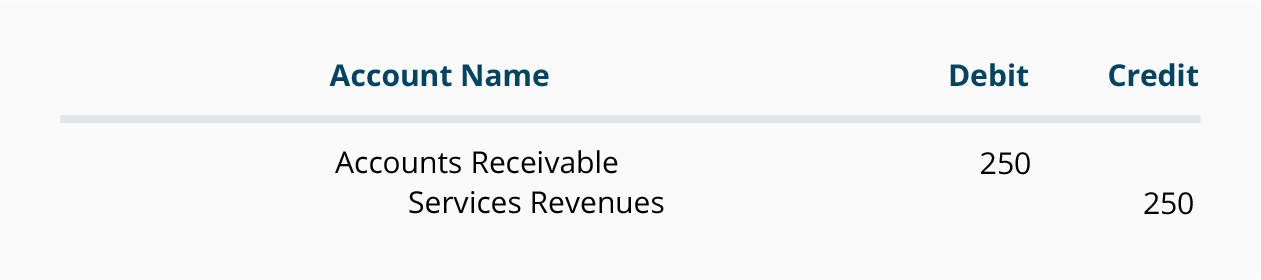

We

know that the unnamed account cannot be Cash because the company did not

receive money on December 3. However, the company has earned the right to

receive the money in seven days. The account title for the money that Direct

Delivery has a right to receive for having provided the service is Accounts

Receivable (an asset account).

Again, reporting revenues

when they are earned results from the basic accounting principle known as the revenue recognition principle.

Sample

Transaction #6

For

simplicity, let's assume that the only expense incurred by Direct Delivery so

far was a fee to a temporary help agency for a person to help Joe deliver

parcels on December 3. The temp agency fee is $80 and is due by December 12.

If a company does not pay

cash immediately, you cannot credit Cash. But because the company owes someone

the money for its purchase, we say it has an obligation or liability to pay. Most accounts involved with

obligations have the word "payable" in their name, and one of the

most frequently used accounts is Accounts Payable. Also keep in mind that

expenses are almost always debited.

The

accounts and amounts for the temporary help are:

Here's a Tip

Expenses

are (almost) always debited.

Here's a Tip

If

a company does not pay cash right away for an expense or for an asset, you

cannot credit Cash. Because the company owes someone

the money for its purchase, we say it has an obligation or liability to pay.

The most likely liability account involved in business obligations is Accounts

Payable.

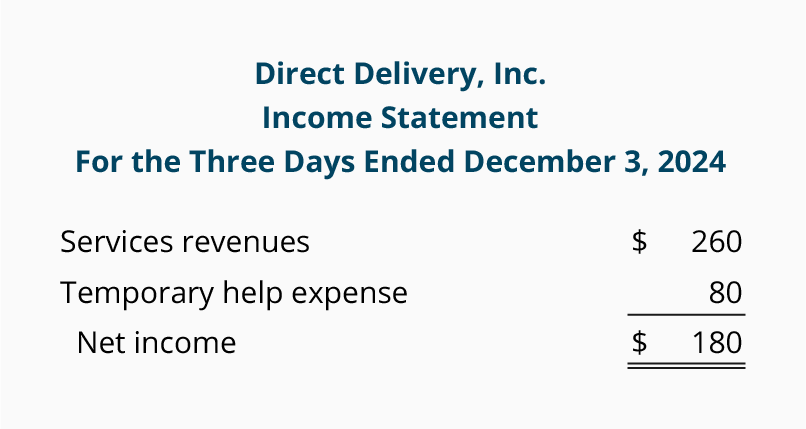

Revenues

and expenses appear on the income statement as shown below:

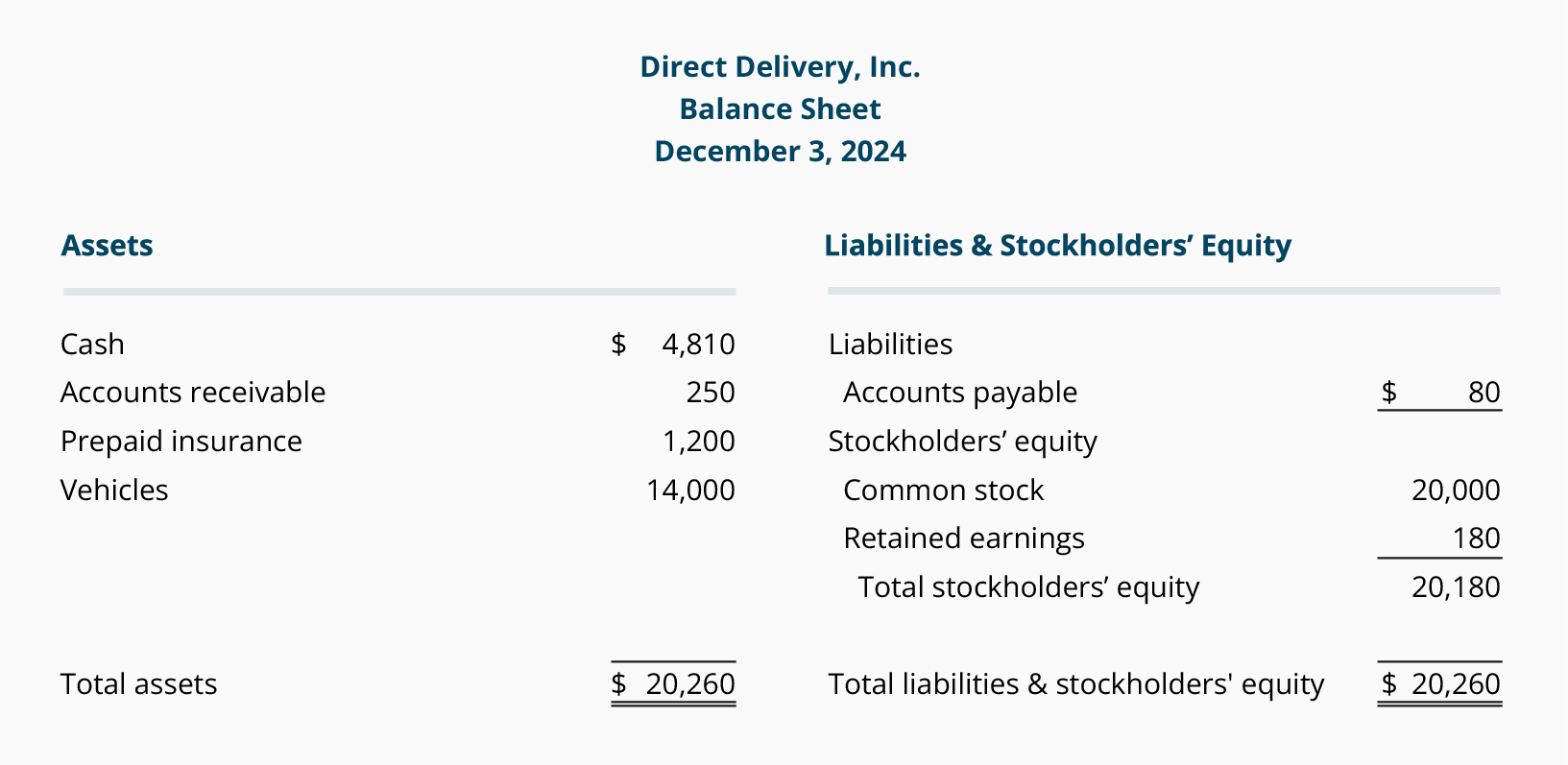

After

the entries through December 3 have been recorded, the balance sheet will look

like this:

Notice that the year-to-date net income (bottom

line of the income statement) increased Stockholders' Equity by the same

amount, $180. This connection between the income statement and balance sheet is

important. For one, it keeps the balance sheet and the accounting equation in

balance. Secondly, it demonstrates that revenues will cause the stockholders'

equity to increase and expenses will cause stockholders' equity to decrease.

After the end of the year financial statements are prepared, you will see that

the income statement accounts (revenue accounts and expense accounts) will be

closed or zeroed out and their balances will be transferred into the Retained Earnings account.

This will mean the revenue and expense accounts will start the new year with

zero balances—allowing the company "to keep score" for the new year.

Marilyn

suggested that perhaps this introduction was enough material for their first

meeting. She wrote out the following notes, summarizing for Joe the important

points of their discussion:

1.

When a company pays cash

for something, the company will credit Cash

and will have to debit a second account. Assuming that a company prepares monthly financial

statements—

§

If the amount is used up or will

expire in the current month, the account to be debited will be an expense

account. (Advertising Expense, Rent Expense, Wages Expense are three examples.)

§

If the amount is not used

up or does not expire

in the current month, the account to be debited will be an asset account.

(Examples are Prepaid Insurance, Supplies,Prepaid Rent, Prepaid Advertising, Prepaid Association Dues, Land, Buildings, andEquipment.)

§

If the amount reduces a company's

obligations, the account to be debited will be a liability account. (Examples

include Accounts Payable, Notes Payable, Wages Payable,and Interest Payable.)

2.

When a company receives cash, the company will debit Cash

and will have to credit another account. Assuming that a company will prepare monthly financial

statements—

§

If the amount received is from a

cash sale, or for a service that has just been performed but has not yet been

recorded, the account to be credited is a revenue account such as Service Revenues or Fees Earned.

§

If the amount received is an

advance payment for a service that has not yet been performed or earned, the

account to be credited is Unearned Revenue.

§

If the amount received is a

payment from a customer for a sale or service delivered earlier and has already

been recorded as revenue, the account to be credited isAccounts Receivable.

§

If the amount received is the

proceeds from the company signing a promissory note, the account to be credited

is Notes Payable.

§

If the amount received is an

investment of additional money by the owner of the corporation, a stockholders'

equity account such as Common Stock is credited.

Note: To learn more about debits and credits, go to Explanation of Debits and Credits and Quiz for Debits and Credits.

3.

Revenues are recorded as Service

Revenues or Sales when the service or sale has been performed, not when

the cash is received. This reflects the basic accounting principle known as the

revenue recognition principle.

4.

Expenses are matched with revenues

or with the period of time shown in the heading of the income statement, not in

the period when the expenses were paid. This reflects the basic accounting

principle known as the matching principle.

5.

The financial statements also

reflect the basic accounting principle known as thecost principle. This

means assets are shown on the balance sheet at their original cost

orless and

not at their current value. The income statement expenses also reflect the cost

principle. For example, the depreciation expense is based on the original cost of

the asset being depreciated and not on the current replacement cost.

Accounting Equation(Explanation)

More ways to study this topic:

Explanation

1.

Part 1

2.

Part

2

3.

Part

3

4.

Part 4

5.

Part

5

6.

Part

6

7.

Part

7

8.

Part

8

9.

Part

9

10. Part

10

11. Part

11

Introduction to the Accounting

Equation

From the large, multi-national corporation down to the

corner beauty salon, every business transaction will have an effect on a

company's financial position. The financial position of a company is measured

by the following items:

- Assets (what

it owns)

- Liabilities

(what it owes to others)

- Owner's

Equity (the difference between assets and liabilities)

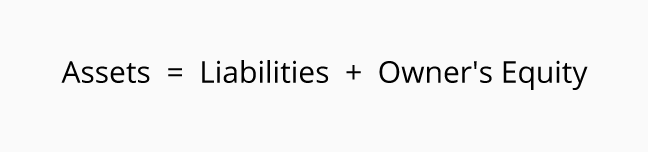

The accounting equation (or basic accounting equation) offers us a simple way

to understand how these three amounts relate to each other. The accounting

equation for a sole proprietorship is:

The accounting equation for a corporation is:

Assets are

a company's resources—things the company owns. Examples of assets include cash,

accounts receivable, inventory, prepaid insurance, investments, land,

buildings, equipment, and goodwill. From the accounting equation, we see that

the amount of assets must equal the combined amount of liabilities plus owner's

(or stockholders') equity.

Liabilities are a company's

obligations—amounts the company owes. Examples of liabilities include notes or

loans payable, accounts payable, salaries and wages payable, interest payable,

and income taxes payable (if the company is a regular corporation). Liabilities

can be viewed in two ways:

(1) as claims by creditors against the company's

assets, and

(2) a source—along with owner or stockholder equity—of the company's assets.

(2) a source—along with owner or stockholder equity—of the company's assets.

Owner's equity or stockholders' equity is the amount left over after liabilities are deducted

from assets:

Assets

- Liabilities = Owner's (or Stockholders') Equity.

Owner's

or stockholders' equity also reports the amounts invested into the company by

the owners plus the cumulative net income of the company that has not been withdrawn or

distributed to the owners.

If

a company keeps accurate records, the accounting equation will always be

"in balance," meaning the left side should always equal the right

side. The balance is maintained becauseevery business

transaction affects at least two of a

company's accounts. For example, when a company

borrows money from a bank, the company's assets will increase and its

liabilities will increase by the same amount. When a company purchases

inventory for cash, one asset will increase and one asset will decrease.

Because there are two or more accounts affected by every transaction, the

accounting system is referred to as double-entry accounting.

A

company keeps track of all of its transactions by recording them in accounts in

the company'sgeneral ledger. Each

account in the general ledger is designated as to its type: asset, liability,

owner's equity, revenue, expense, gain, or loss account.

We

created a visual tutorial to demonstrate how a variety of transactions will

affect the accounting equation and the financial statements. It is available in AccountingCoach PROalong with exam questions that pertain to the accounting equation.

Balance Sheet and Income Statement

The balance sheet is also known as the statement of financial position

and it reflects the accounting equation. The balance sheet reports a company's

assets, liabilities, and owner's (or stockholders') equity at a specific point

in time. Like the accounting equation, it shows that a company's total amount

of assets equals the total amount of liabilities plus owner's (or

stockholders') equity.

The income statement is the financial statement that reports a company's

revenues and expenses and the resulting net income. While the balance sheet is

concerned with one point in time, the income statement covers a time interval or period of

time. The income statement will explain part of the change in the owner's or

stockholders' equity during the time interval between two balance sheets.

Examples

In our examples in the following pages of this topic, we show how a given transaction affects the accounting equation. We also show how the same transaction affects specific accounts by providing the journal entry that is used to record the transaction in the company's general ledger.

In our examples in the following pages of this topic, we show how a given transaction affects the accounting equation. We also show how the same transaction affects specific accounts by providing the journal entry that is used to record the transaction in the company's general ledger.

Our

examples will show the effect of each transaction on the balance sheet and

income statement. Our examples also assume that the accrual basis of accounting is being followed.

Parts 2 - 6 illustrate transactions involving a sole

proprietorship.

Parts 7 - 10 illustrate almost identical transactions

as they would take place in a corporation.

Accounting Equation for a Sole Proprietorship: Transactions 1–2

We

present nine transactions to illustrate how a company's accounting equation

stays in balance.

When a company records a

business transaction, it is not entered into an accounting equation,per se.

Rather, transactions are recorded into specific accounts contained in the

company's general ledger. Each account is designated as an asset, liability,

owner's equity, revenue, expense, gain, or loss account. The general ledger accounts

are then used to prepare the balance sheets and income statements throughout

the accounting periods.

In

the examples that follow, we will use the following accounts:

- Cash

- Accounts Receivable

- Equipment

- Notes Payable

- Accounts Payable

- J. Ott, Capital

- J. Ott, Drawing

- Service Revenues

- Advertising Expense

- Temp Service Expense

(To view a more complete

listing of accounts for recording transactions, see theExplanation of Chart of Accounts.)

Sole

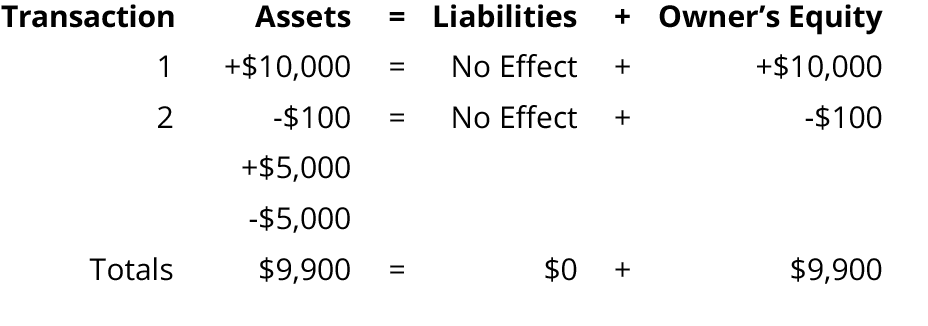

Proprietorship Transaction #1.

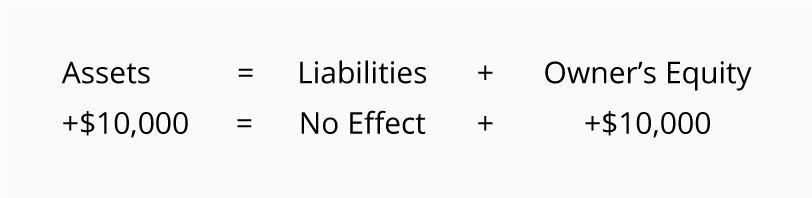

Let's

assume that J. Ott forms a sole proprietorship called Accounting Software Co.

(ASC). On December 1, 2014, J. Ott invests personal funds of $10,000 to start

ASC. The effect of this transaction on ASC's accounting equation is:

As

you can see, ASC's assets increase by $10,000 and so does ASC's owner's equity.

As a result, the accounting equation will be in balance.

You

can interpret the amounts in the accounting equation to mean that ASC has

assets of $10,000 and the source of those assets was the owner, J. Ott.

Alternatively, you can view the accounting equation to mean that ASC has assets

of $10,000 and there are no claims by creditors (liabilities) against the

assets. As a result, the owner has a claim for the remainder or residual of

$10,000.

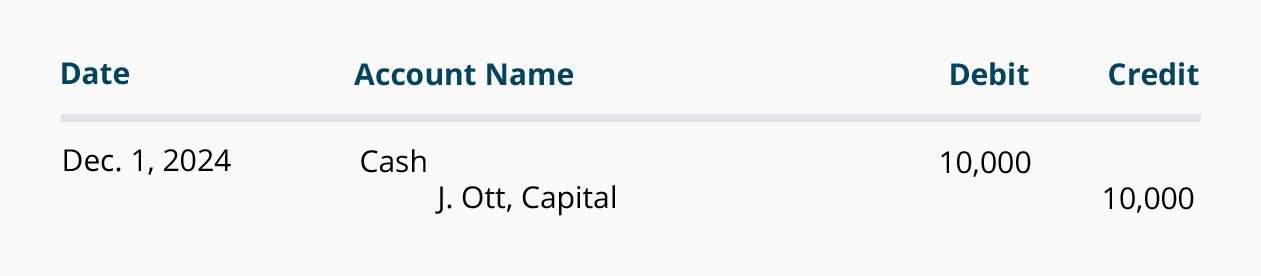

This

transaction is recorded in the asset account Cash and the owner's equity

account J. Ott, Capital. The general journal entry to record the transactions

in these accounts is:

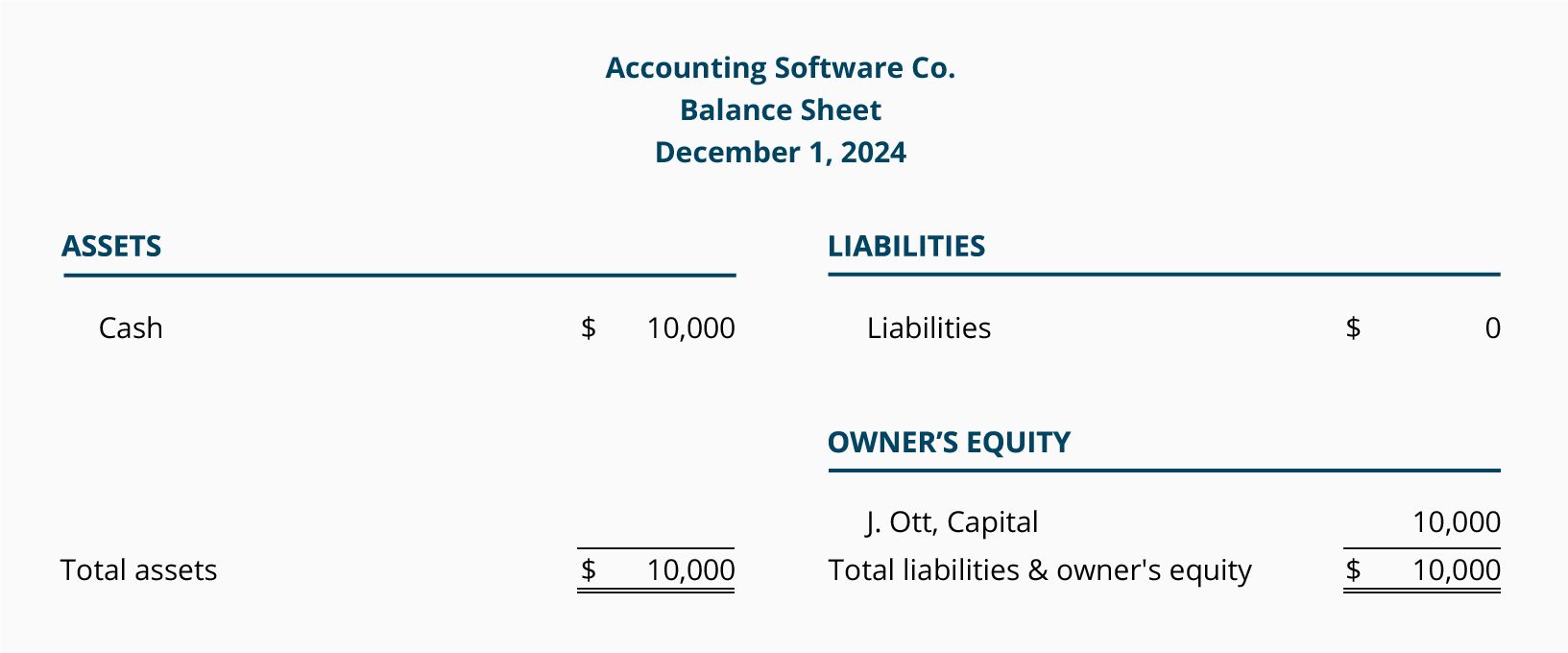

After

the journal entry is recorded in the accounts, a balance sheet can be prepared

to show ASC's financial position at the end of December 1, 2014:

The

purpose of an income statement is to report revenues and expenses. Since ASC

has not yet earned any revenues nor incurred any expenses, there are no

transactions to be reported on an income statement.

Sole

Proprietorship Transaction #2.

On

December 2, 2014 J. Ott withdraws $100 of cash from the business for his

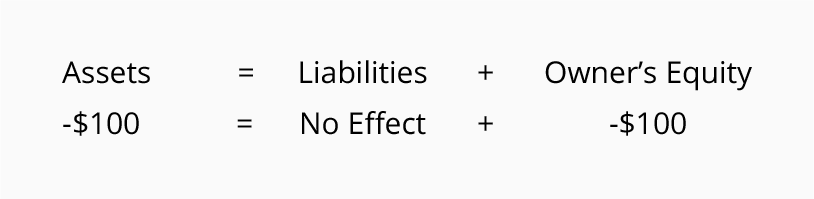

personal use. The effect of this transaction on ASC's accounting equation is:

The

accounting equation remains in balance since ASC's assets have been reduced by

$100 and so has the owner's equity.

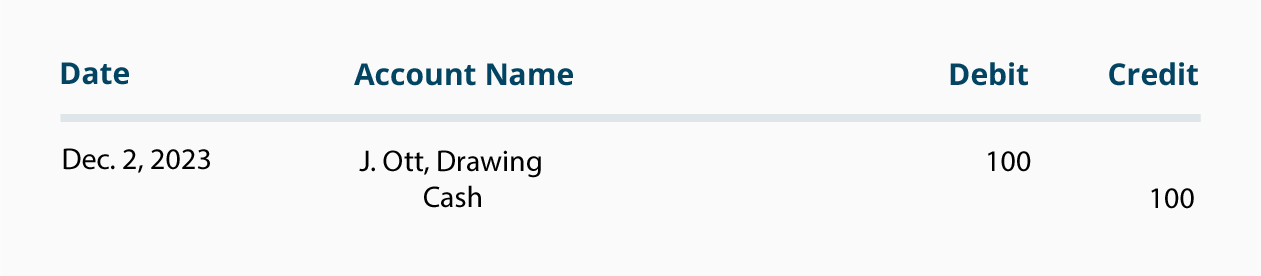

This

transaction is recorded in the asset account Cash and the owner's equity

account J. Ott, Drawing. The general journal entry to record the transactions

in these accounts is:

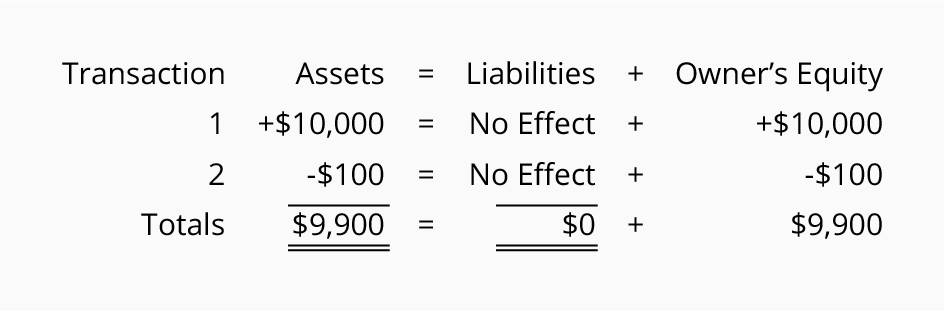

Since

the transactions of December 1 and 2 were each in balance, the sum of both transactions

should also be in balance:

The

totals indicate that ASC has assets of $9,900 and the source of those assets is

the owner of the company. You can also conclude that the company has assets or

resources of $9,900 and the only claim against those resources is the owner's

claim.

The

December 2 balance sheet will communicate the company's financial position as

of midnight on December 2:

Withdrawals

of company assets by the owner for the owner's personal use are known as

"draws." Since draws are not expenses, the transaction is not

reported on the company's income statement.

Accounting Equation for a Sole Proprietorship: Transactions 3–4

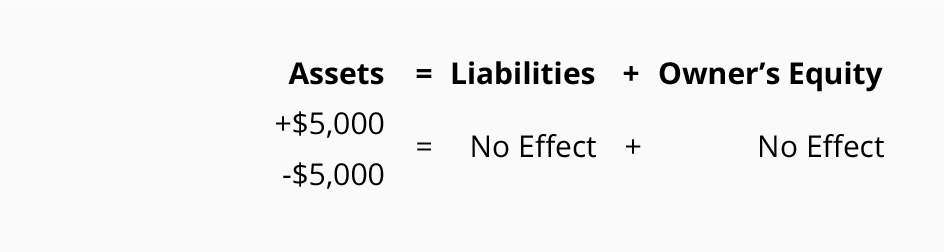

Sole

Proprietorship Transaction #3.

On

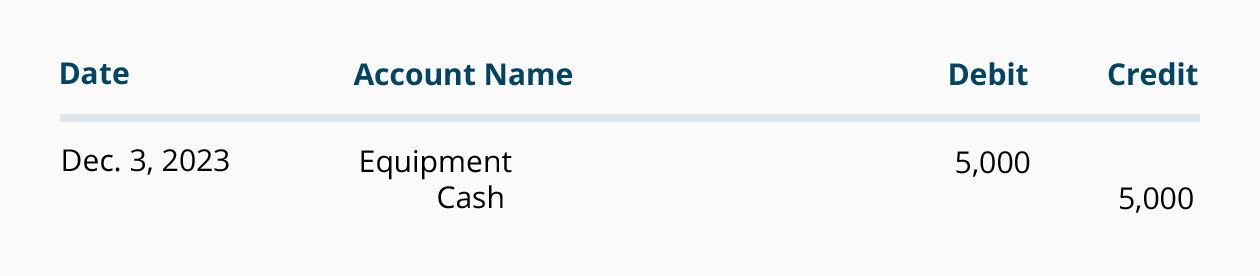

December 3, 2014 Accounting Software Co. spends $5,000 of cash to purchase computer

equipment for use in the business. The effect of this transaction on the

accounting equation is:

The

accounting equation reflects that one asset increases and another asset

decreases. Since the amount of the increase is the same as the amount of the

decrease, the accounting equation remains in balance.

This

transaction is recorded in the asset accounts Equipment and Cash. Equipment

increases by $5,000, and Cash decreases by $5,000. The general journal entry to

record the transactions in these accounts is:

The

combined effect of the first three transactions is shown here:

The

totals tell us that the company has assets of $9,900 and the source of those

assets is the owner of the company. It also tells us that the company has

assets of $9,900 and the only claim against those assets is the owner's claim.

The

balance sheet dated December 3, 2014 will reflect the financial position as of

midnight on December 3:

The purchase of equipment

is not an immediate expense. It will become part ofdepreciation expense only

after it is placed into service. We will assume that as of December 3 the

equipment has not been placed into service, therefore, no expense will appear

on an income statement for the period of December 1 through December 3.

Sole

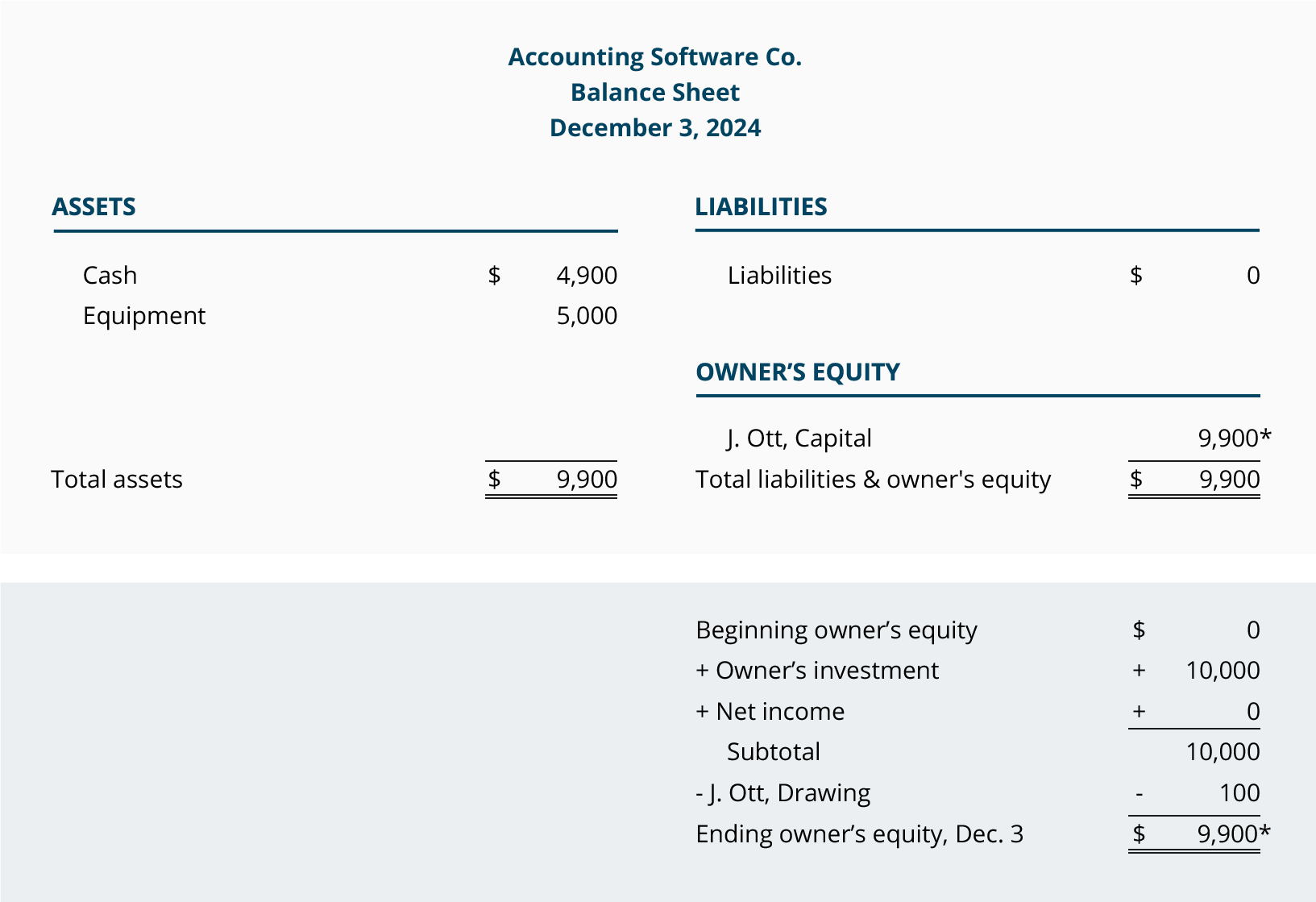

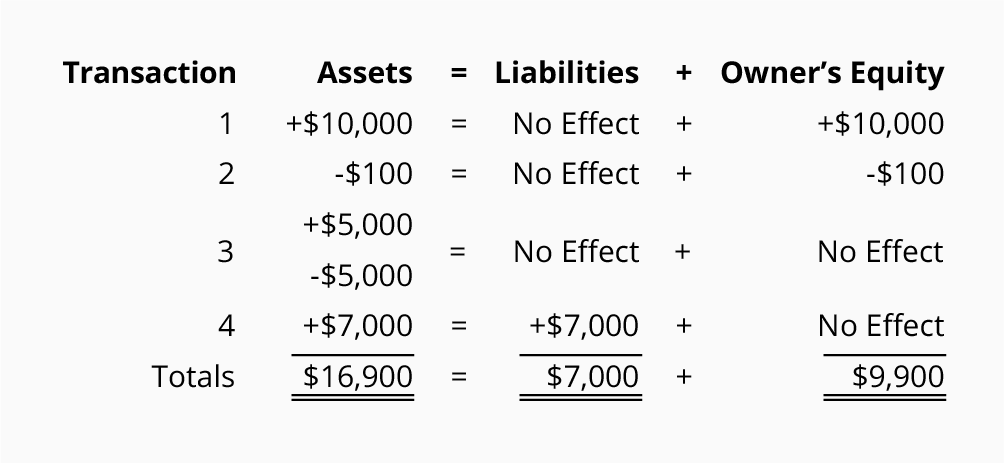

Proprietorship Transaction #4.

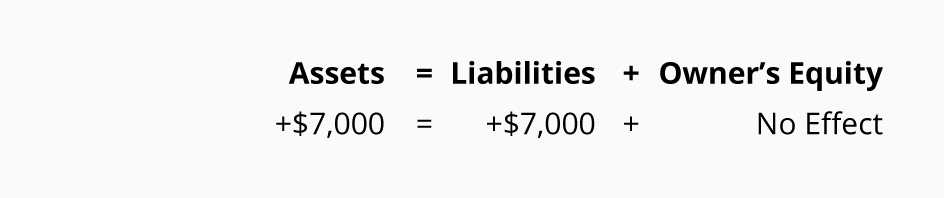

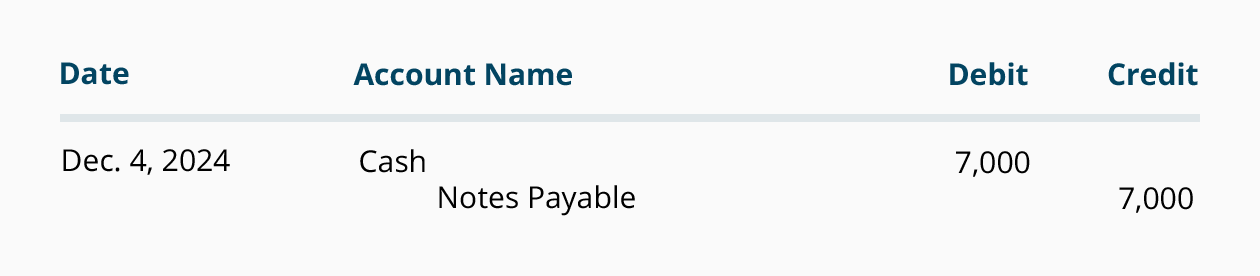

On

December 4, 2014 ASC obtains $7,000 by borrowing money from its bank. The

effect of this transaction on the accounting equation is:

As

you can see, ASC's assets increase and ASC's liabilities increase by $7,000.

This

transaction is recorded in the asset account Cash and the liability account

Notes Payable as shown in this accounting entry:

The

combined effect on the accounting equation from the first four transactions is

available here:

The

totals indicate that the transactions through December 4 result in assets of

$16,900. There are two sources for those assets—the creditors provided $7,000

of assets, and the owner of the company provided $9,900. You can also interpret

the accounting equation to say that the company has assets of $16,900 and the

lenders have a claim of $7,000 and the owner has a claim for the remainder.

The

balance sheet dated December 4 will report ASC's financial position as of that

date:

The

proceeds of the bank loan are not considered to be revenue since ASC did not

earn the money by providing services, investing, etc. As a result, there is no

income statement effect from this transaction.

Accounting Equation for a Sole Proprietorship: Transactions 5–6

Sole

Proprietorship Transaction #5.

On

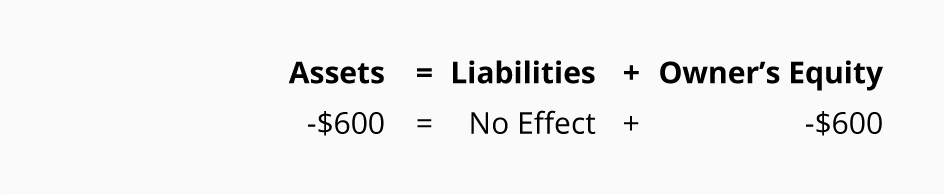

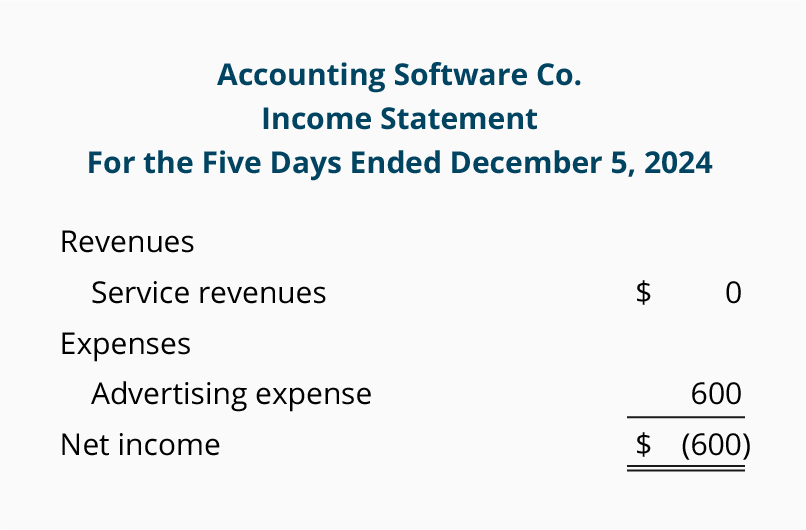

December 5, 2014 Accounting Software Co. pays $600 for ads that were run in

recent days. The effect of this advertising transaction on the accounting

equation is:

Since ASC is paying $600, its assets decrease. The second

effect is a $600 decrease in owner's equity, because the transaction involves

an expense. (An expense is a cost that is used up or its future economic value

cannot be measured.)

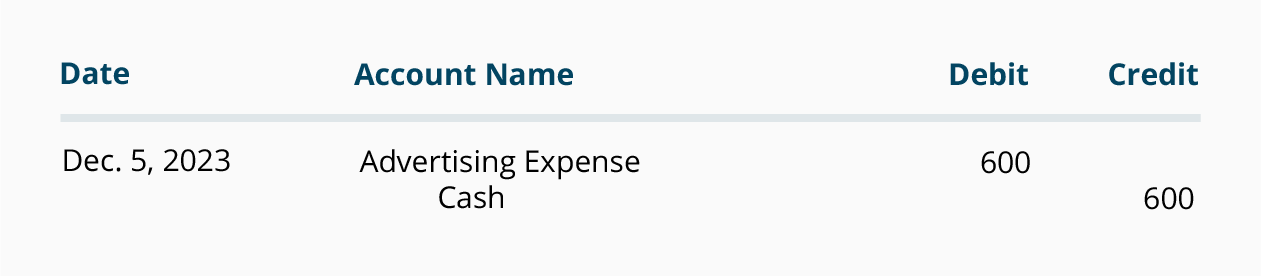

Although

owner's equity is decreased by an expense, the transaction is not recorded

directly into the owner's capital account at this time. Instead, the amount is

initially recorded in the expense account Advertising Expense and in the asset

account Cash.

The

general journal entry to record the transaction is:

The

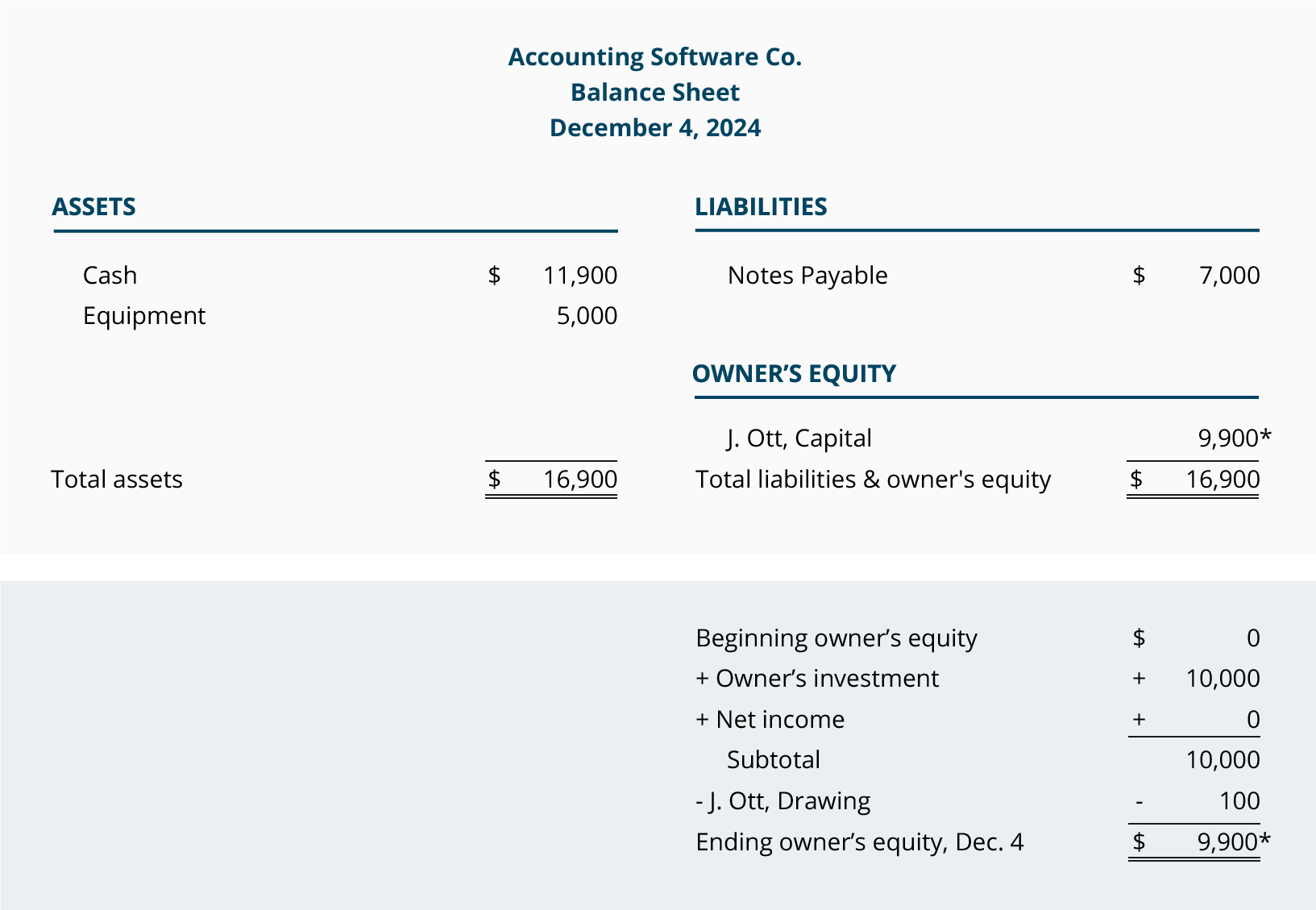

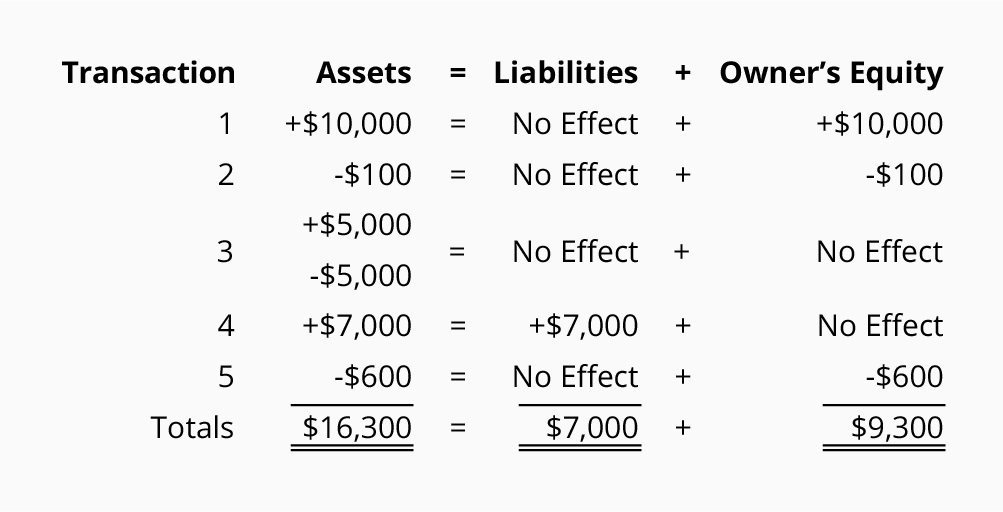

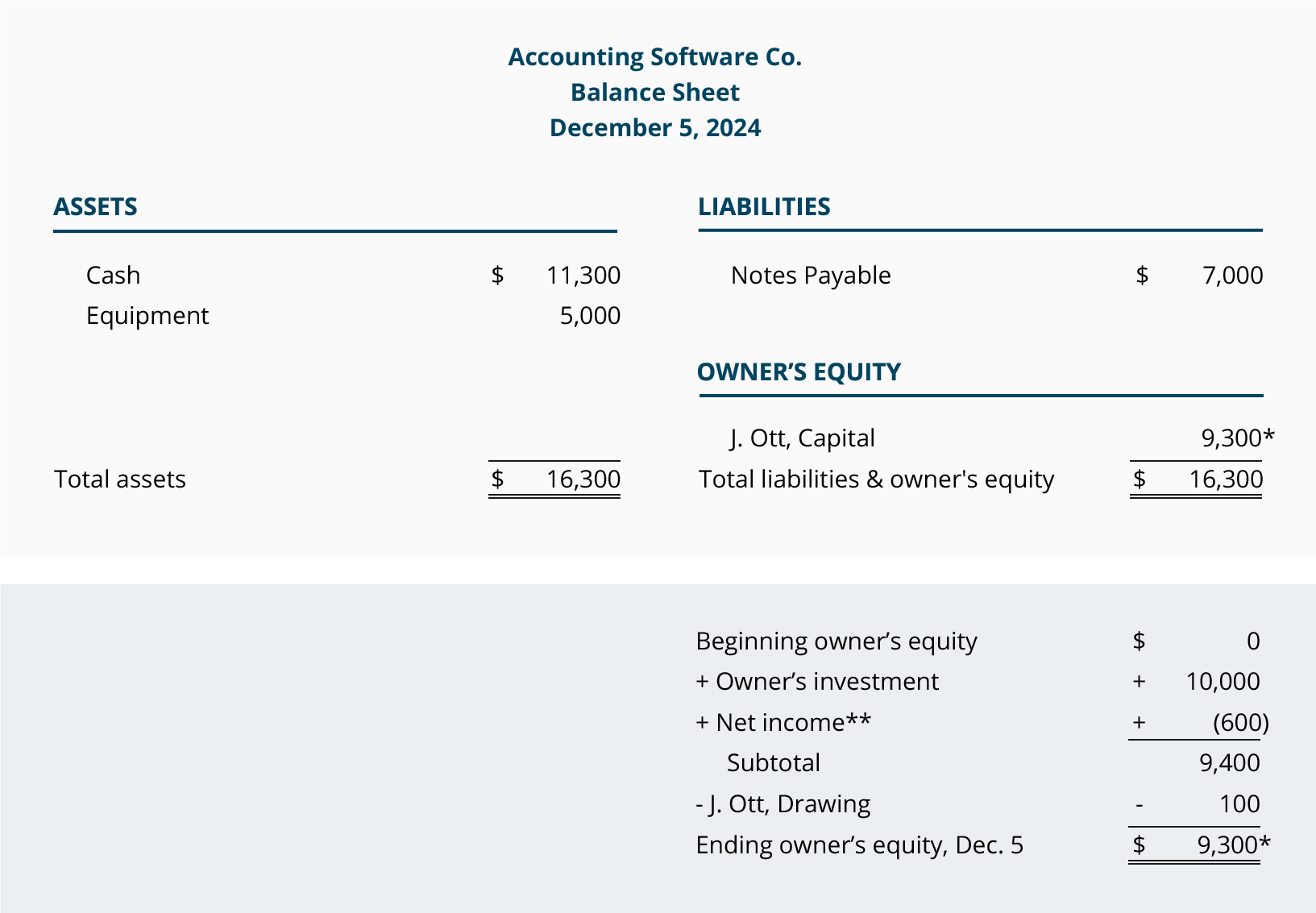

combined effect of the first five transactions is available here:

The

totals now indicate that Accounting Software Co. has assets of $16,300. The

creditors provided $7,000 and the owner of the company provided $9,300. Viewed

another way, the company has assets of $16,300 with the creditors having a

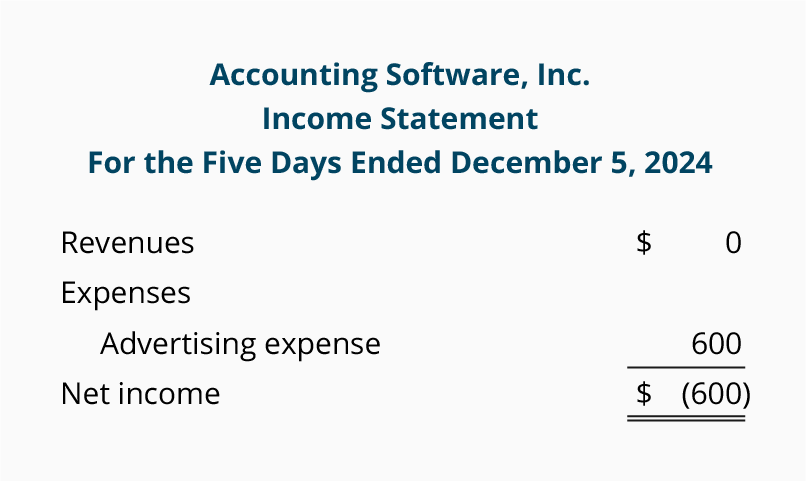

claim of $7,000 and the owner having a residual claim of $9,300.

The

balance sheet as of the end of December 5, 2014 is:

**The

income statement (which reports the company's revenues, expenses, gains, and

losses during a specified time interval) is a link between balance sheets. It

provides the results of operations—an important part of the change in owner's

equity.

Since

this transaction involves an expense, it will involve ASC's income statement.

The company's income statement for the first five days of December is:

Sole

Proprietorship Transaction #6.

On

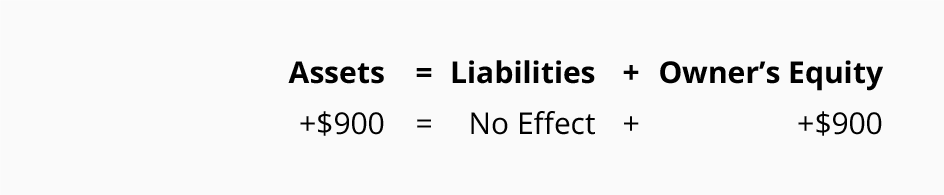

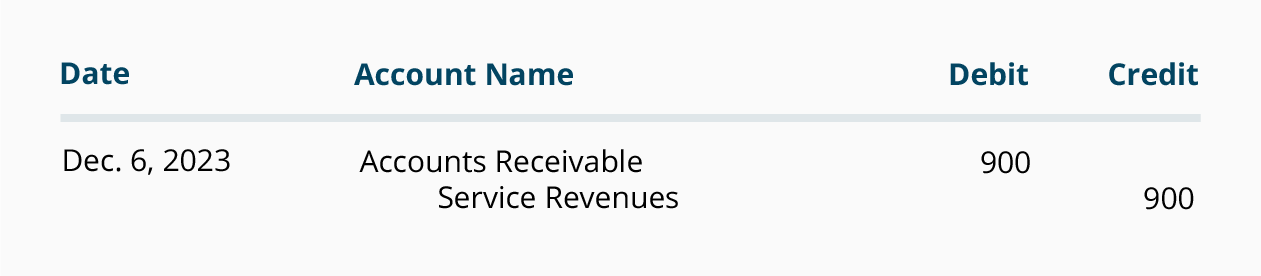

December 6, 2014 ASC performs consulting services for its clients. The clients

are billed for the agreed upon amount of $900. The amounts are due in 30 days.

The effect on the accounting equation is:

Since ASC has performed the

services, it has earned revenues and it has the right to

receive $900 from the clients. This right (known as an account receivable)

causes assets to increase. The earning of revenues causes owner's equity to

increase.

Although

revenues cause owner's equity to increase, the revenue transaction is not

recorded into the owner's capital account at this time. Rather, the amount

earned is recorded in the revenue account Service Revenues. This will allow the

company to report the revenues on its income statement at any time. (After the

year ends, the amount in the revenue account will be transferred to the owner's

capital account.)

The

general journal entry to record the transaction is:

The

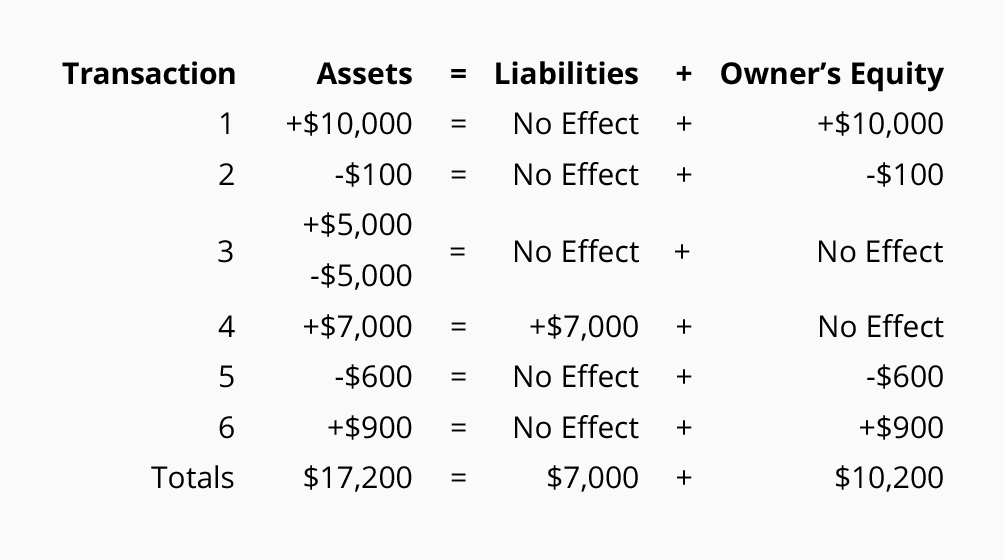

combined effect of the first six transactions can be viewed here:

The

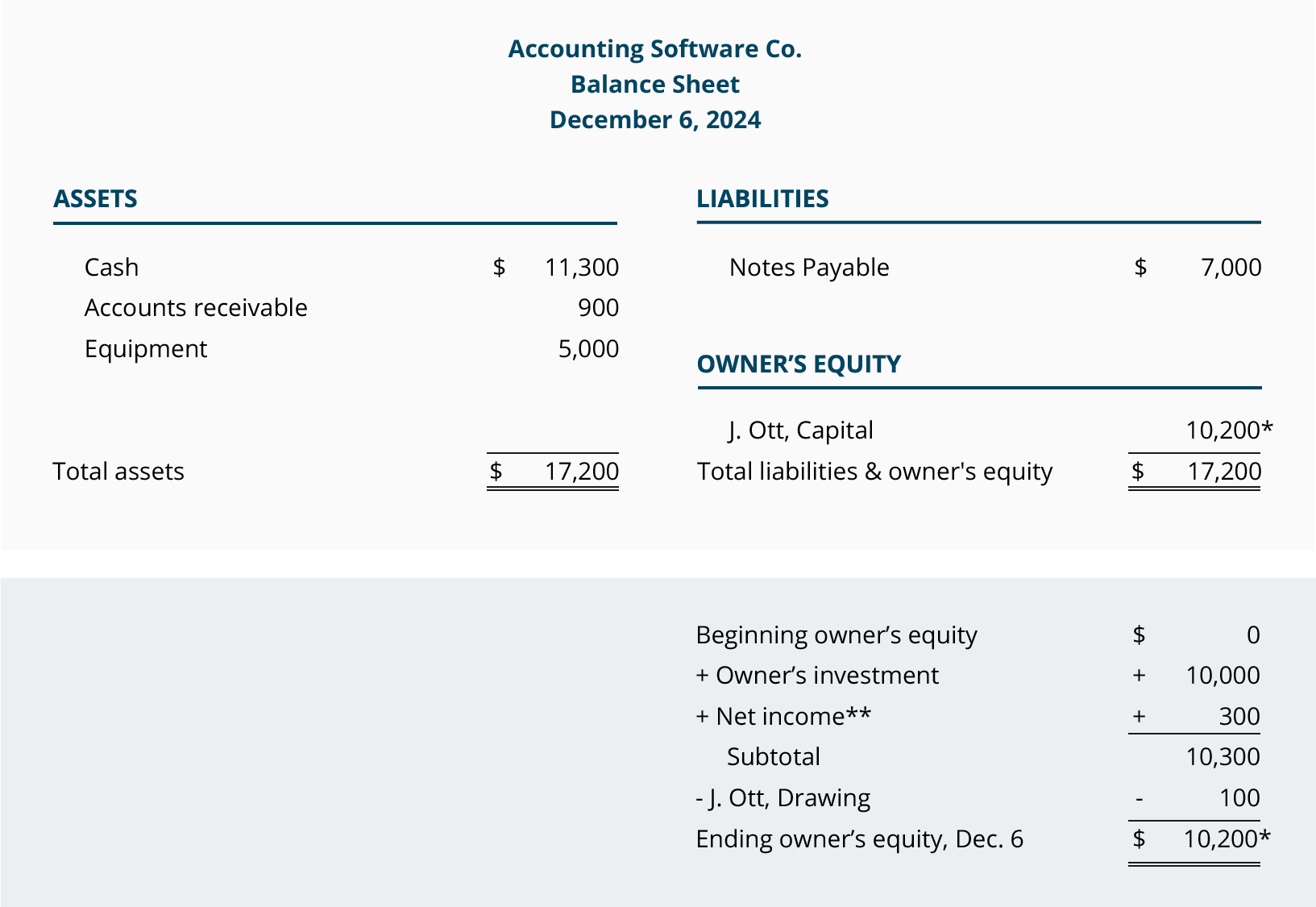

totals tell us that at the end of December 6, the company has assets of

$17,200. It also shows the sources of the assets: creditors providing $7,000

and the owner of the company providing $10,200. The totals also reveal that the

company has assets of $17,200 and the creditors have a claim of $7,000 and the

owner has a claim for the remaining $10,200.

Below

is the balance sheet as of midnight on December 6:

**The

income statement (which reports the company's revenues, expenses, gains, and

losses during a specified time interval) is a link between balance sheets. It

provides the results of operations—an important part of the change in owner's

equity.

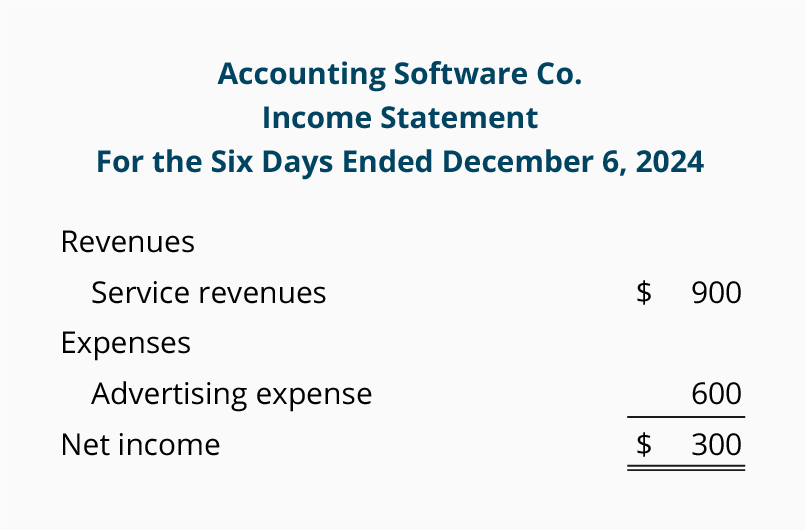

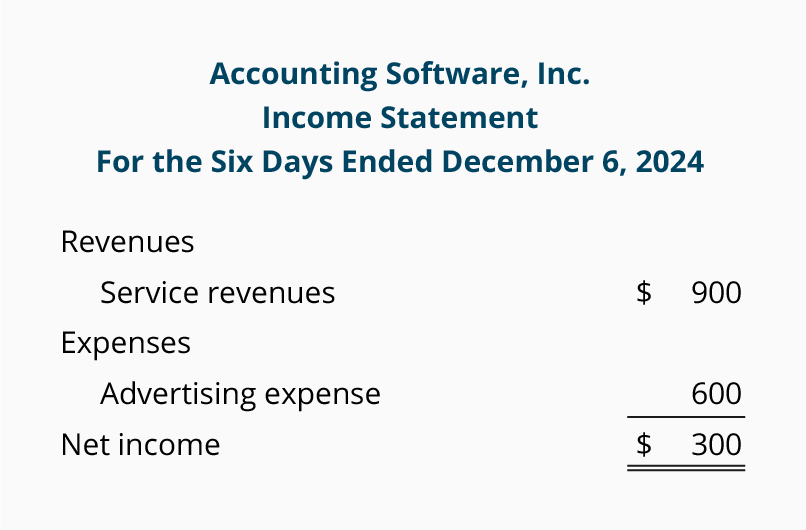

The

Income Statement for Accounting Software Co. for the period of December 1

through December 6 is:

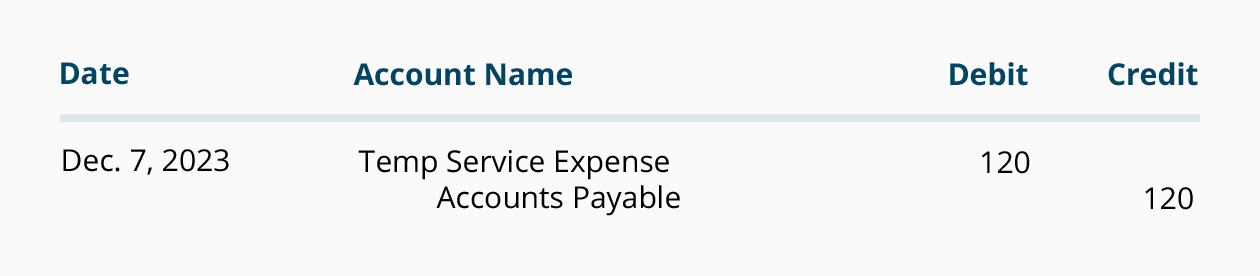

Accounting Equation for a Sole Proprietorship: Transactions 7–8

Sole

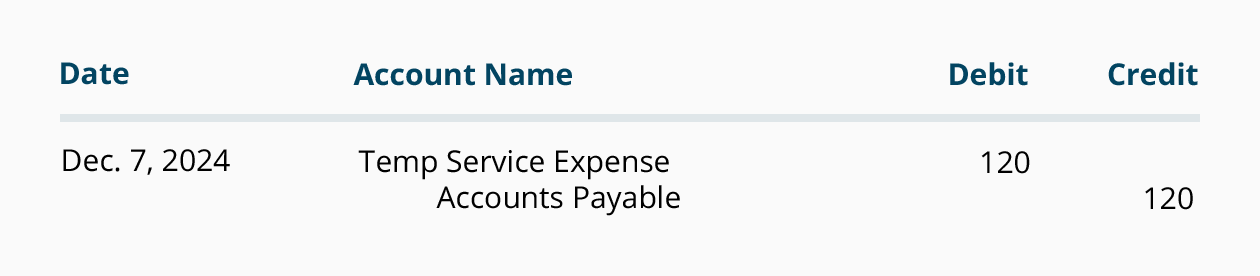

Proprietorship Transaction #7.

On

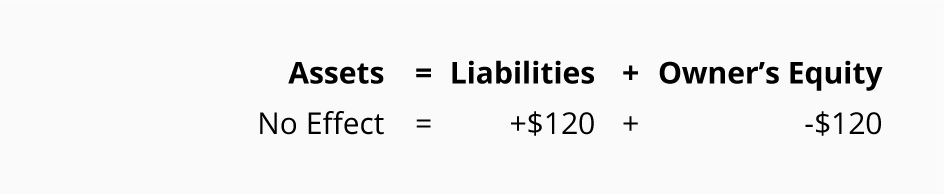

December 7, 2014 ASC uses a temporary help service for 6 hours at a cost of $20

per hour. ASC will pay the invoice when it is due in 10 days. The effect on its

accounting equation is:

ASC's

liabilities increase by $120 and the expense causes owner's equity to decrease

by $120.

The

liability will be recorded in Accounts Payable and the expense will be reported

in Temp Service Expense. The journal entry for recording the use of the temp

service is:

The

effect of the first seven transactions on the accounting equation can be viewed

here:

The

totals show us that the company has assets of $17,200 and the sources are the

creditors with $7,120 and the owner of the company with $10,080. The accounting

equation totals also tell us that the company has assets of $17,200 with the

creditors having a claim of $7,120. This means that the owner's residual claim

is $10,080.

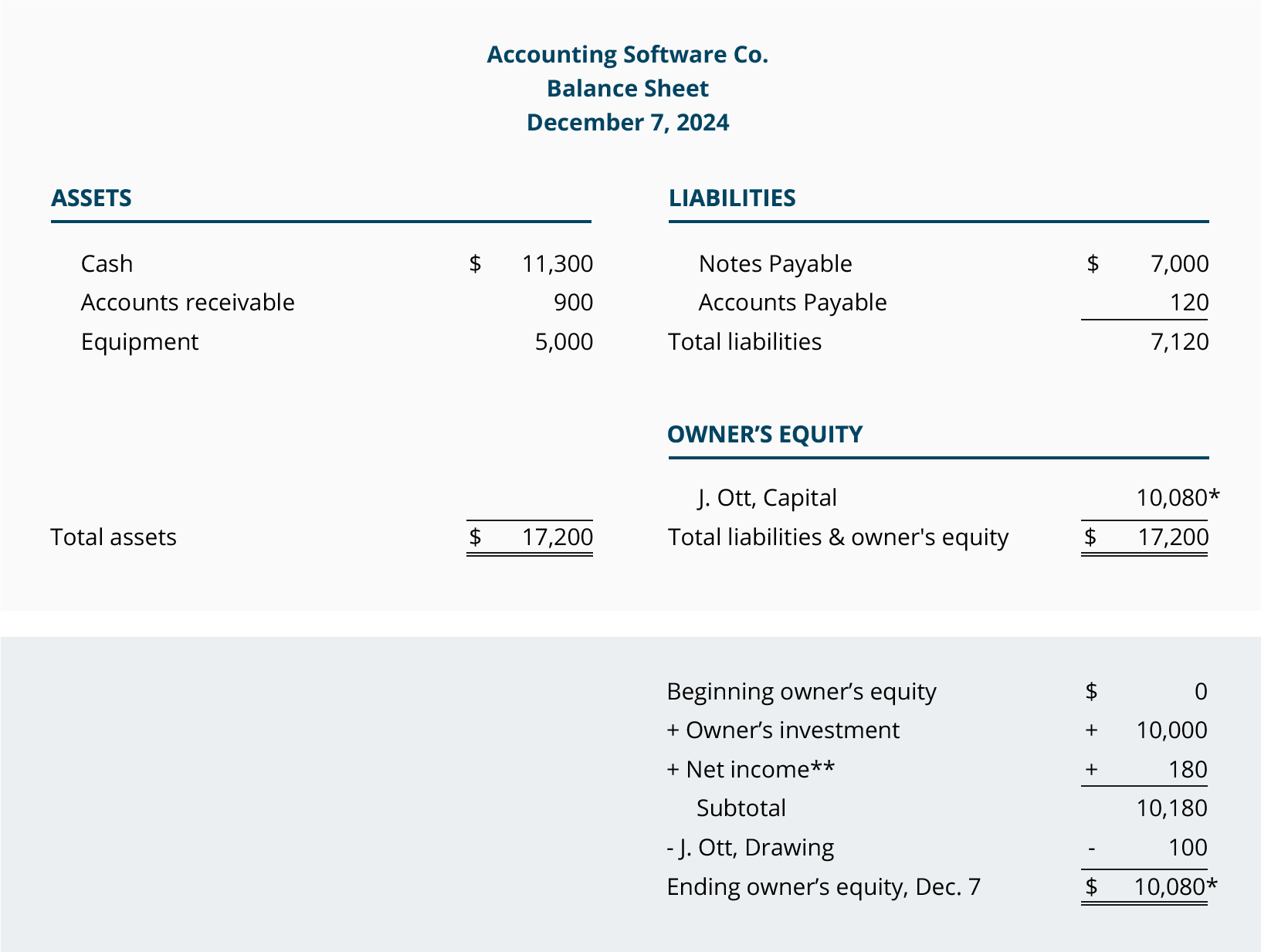

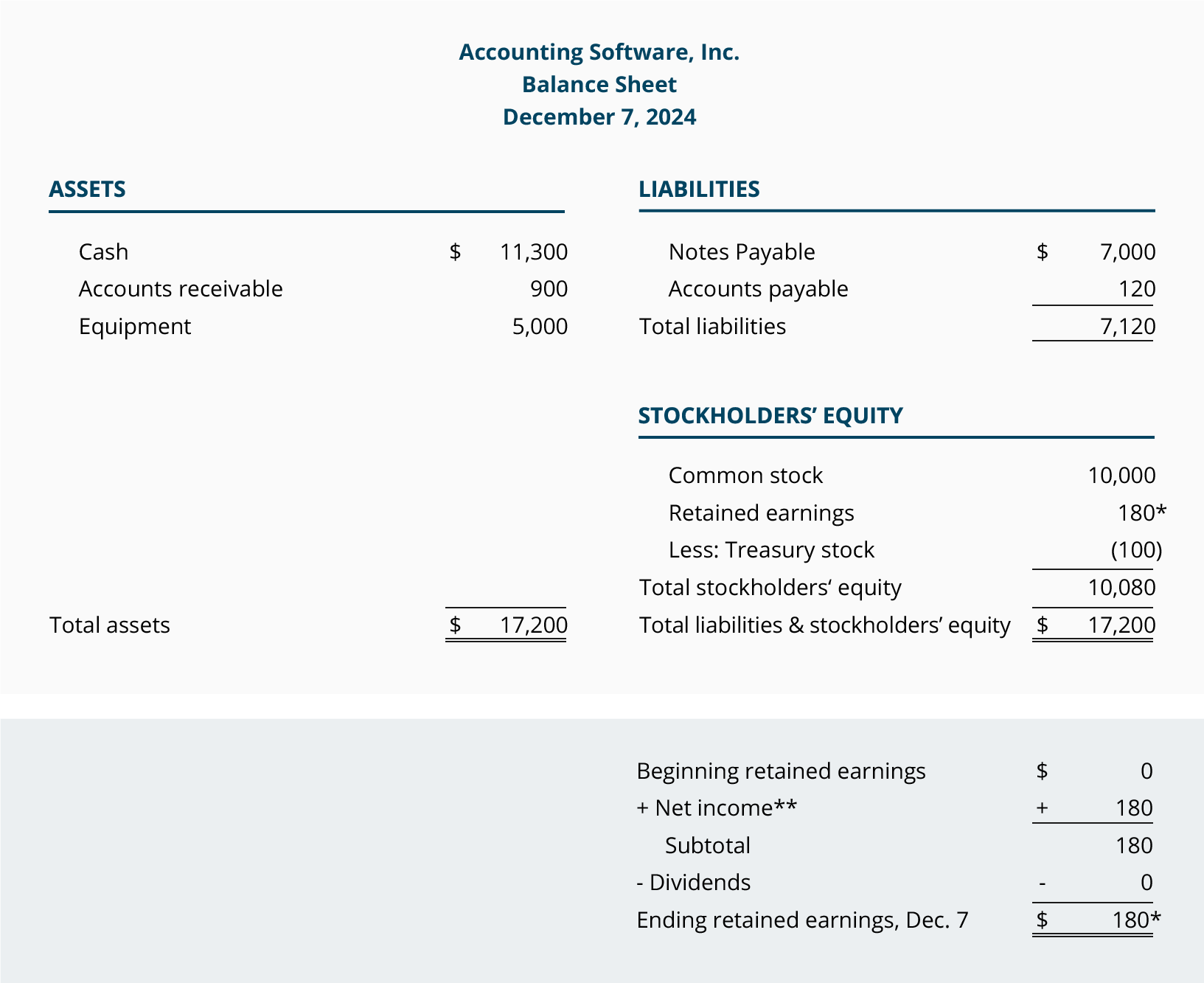

The

financial position of ASC as of midnight on December 7, 2014 is:

**The

income statement (which reports the company's revenues, expenses, gains, and

losses for a specified time interval) is a link between balance sheets. It

provides the results of operations—an important part of the change in owner's

equity.

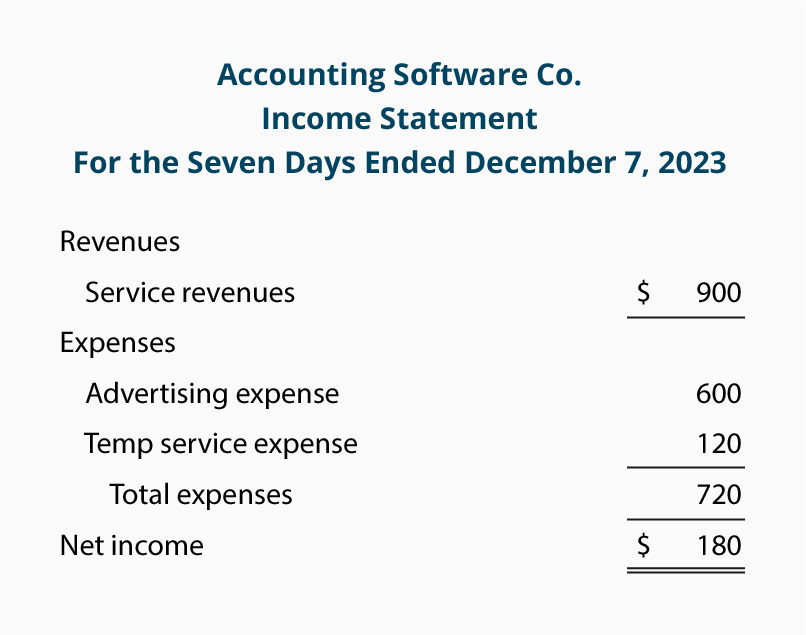

Accounting

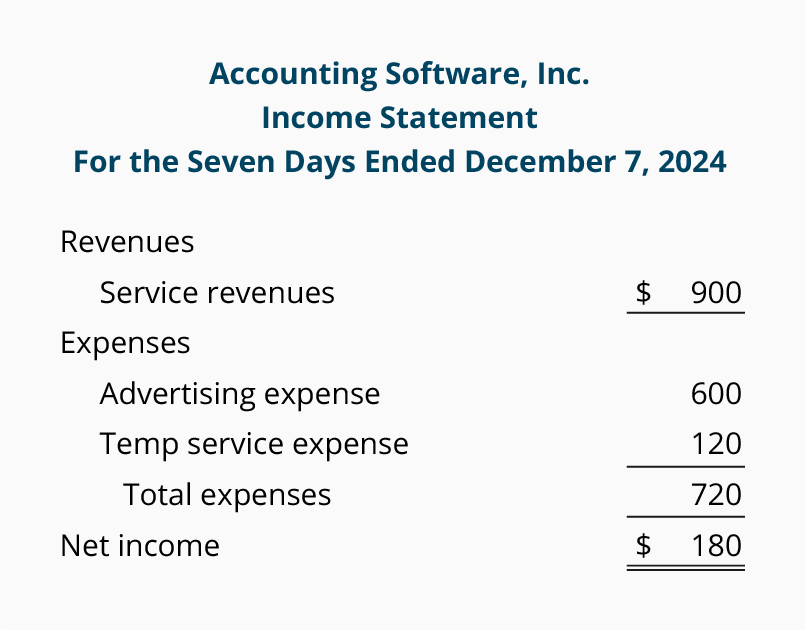

Software Co.'s income statement for the first seven days of December is:

Sole

Proprietorship Transaction #8.

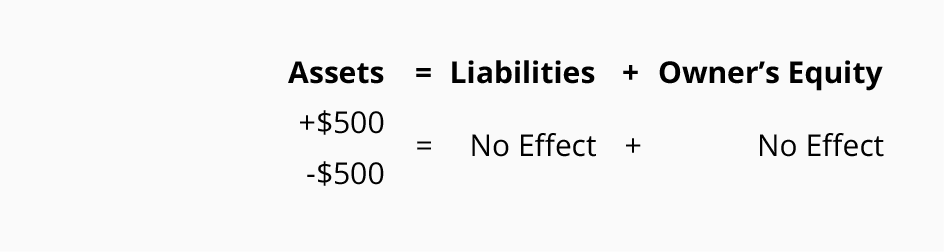

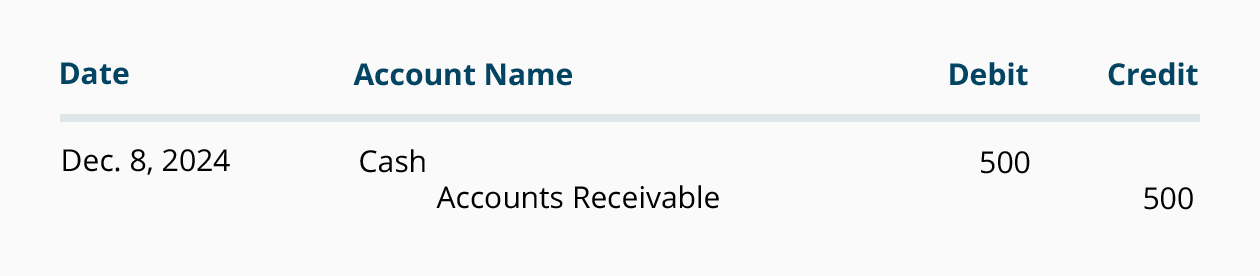

On

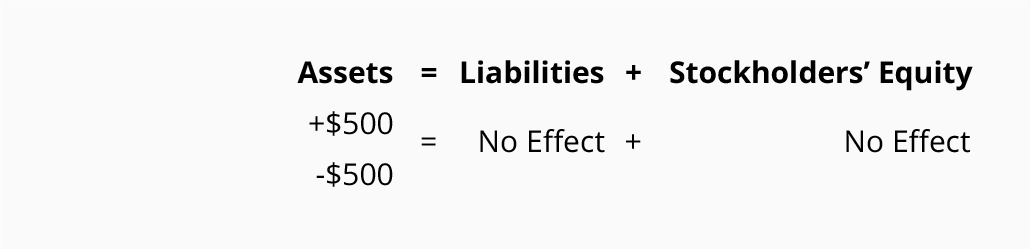

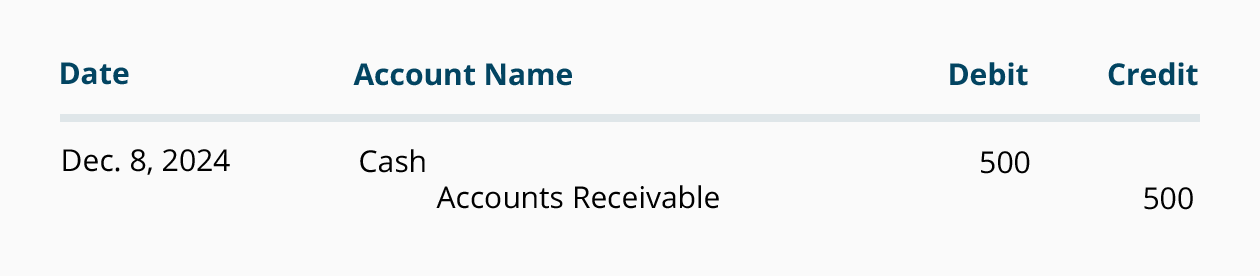

December 8, 2014 ASC receives $500 from the clients it had billed on December

6, 2014. The collection of accounts receivables has this effect on the

accounting equation:

The

company's asset (cash) increases and another asset (accounts receivable)

decreases. Liabilities and owner's equity are unaffected. (There are no

revenues on this date. The revenues were recorded when they were earned on

December 6.)

The

general journal entry to record the increase in Cash, and the decrease in

Accounts Receivable is:

The

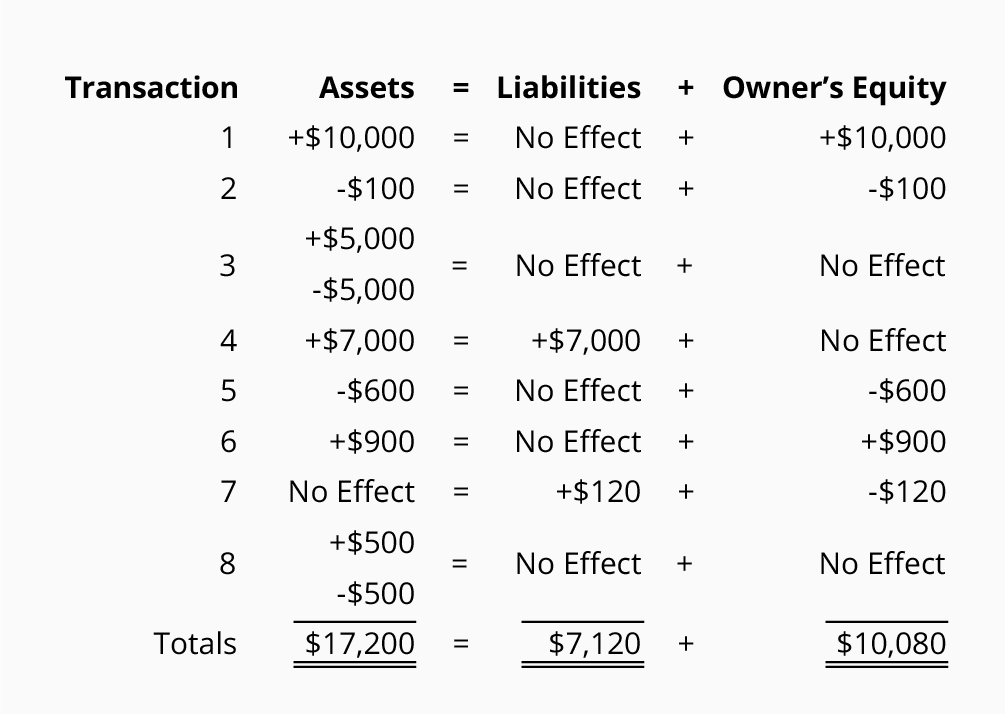

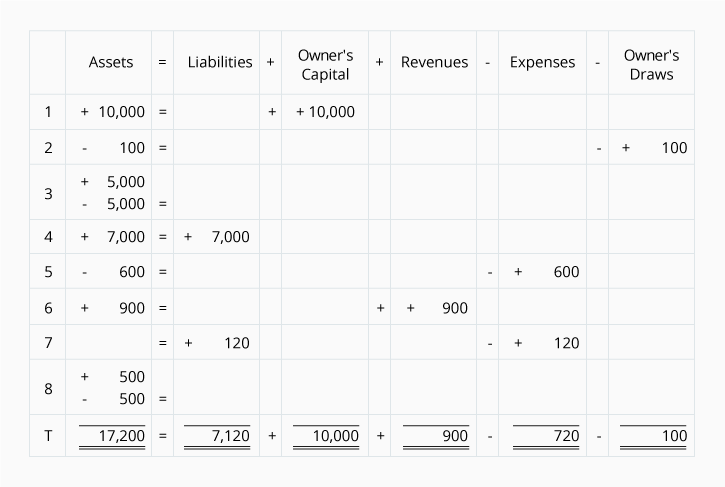

combined effect of the first eight transactions is shown here:

The

totals for the first eight transactions indicate that the company has assets of

$17,200. The creditors provided $7,120 and the owner provided $10,080. The

accounting equation also indicates that the company's creditors have a claim of

$7,120 and the owner has a residual claim of $10,080.

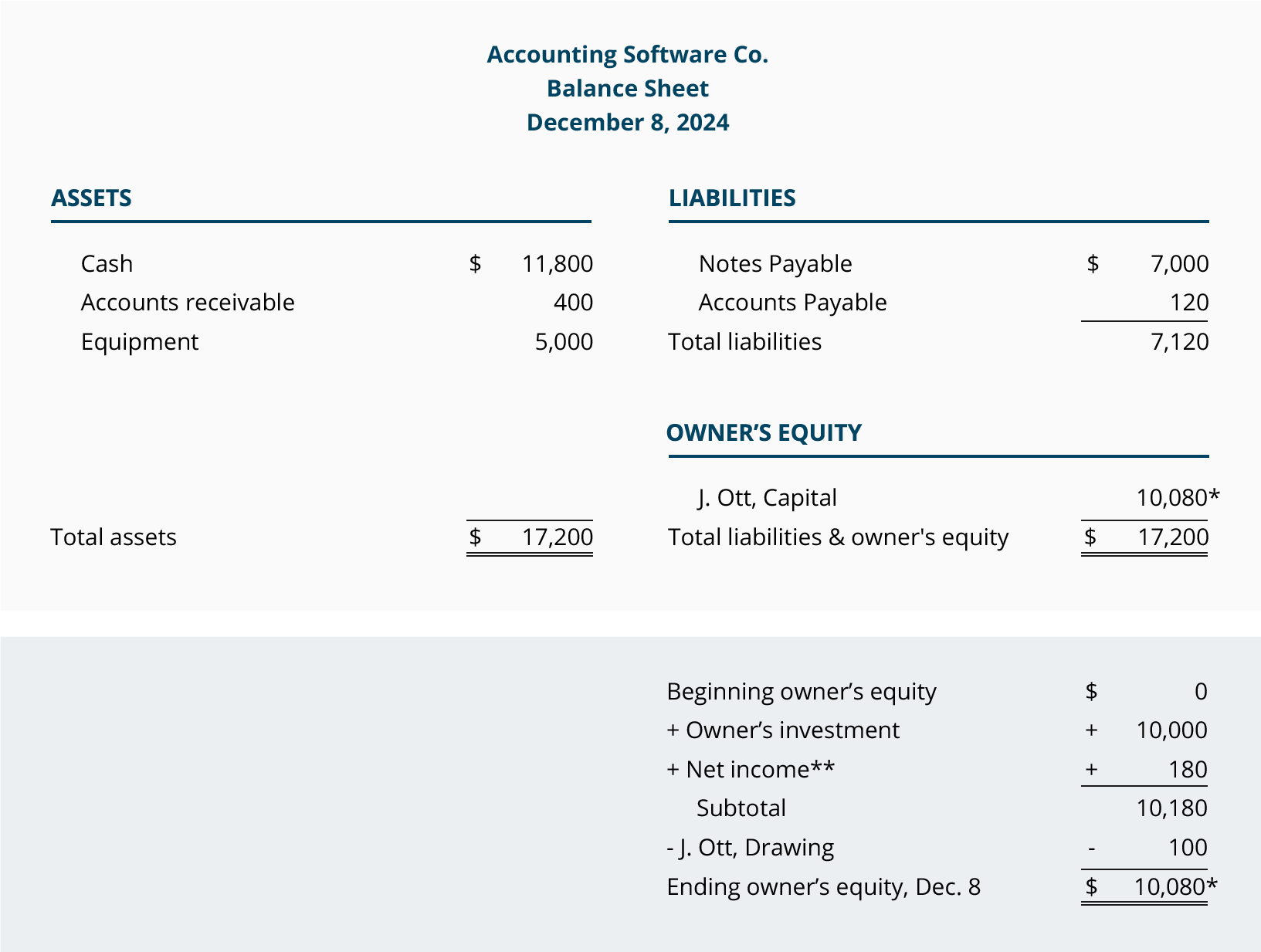

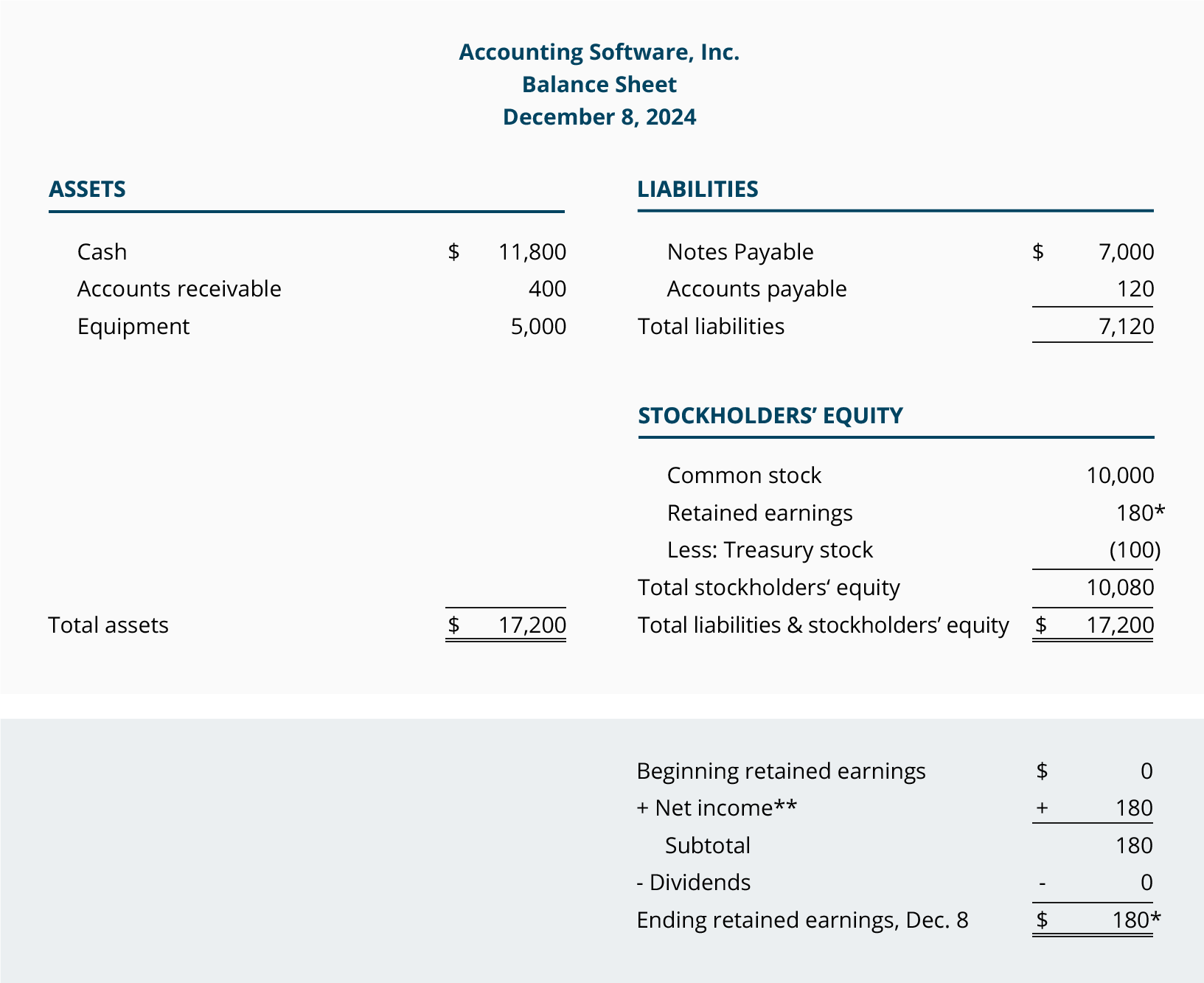

ASC's

balance sheet as of midnight December 8, 2014 is:

**The

income statement (which reports the company's revenues, expenses, gains, and

losses during a specified period of time) is a link between balance sheets. It

provides the results of operations—an important part of the change in owner's

equity.

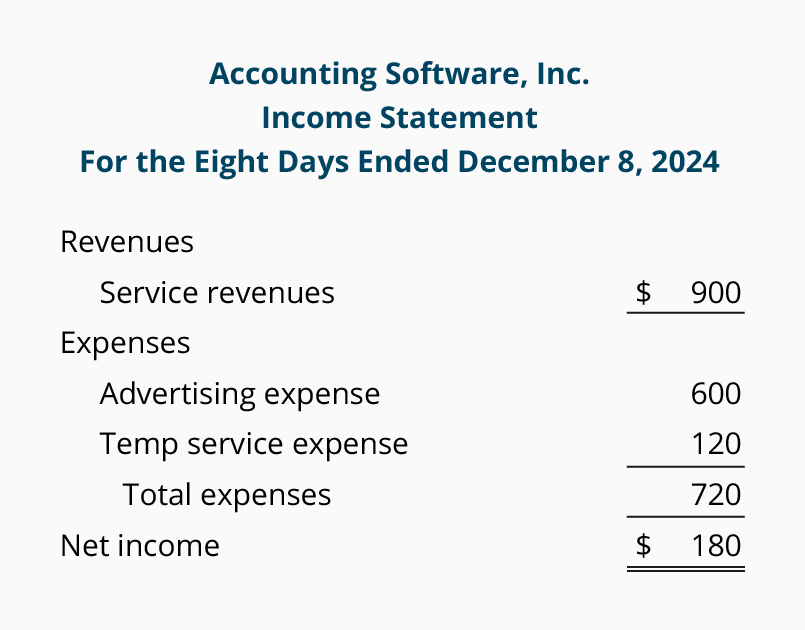

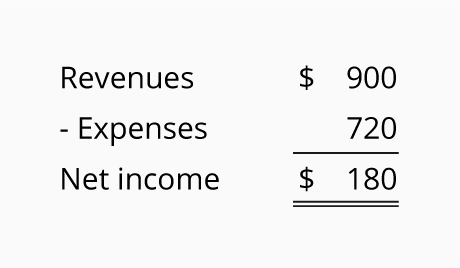

The

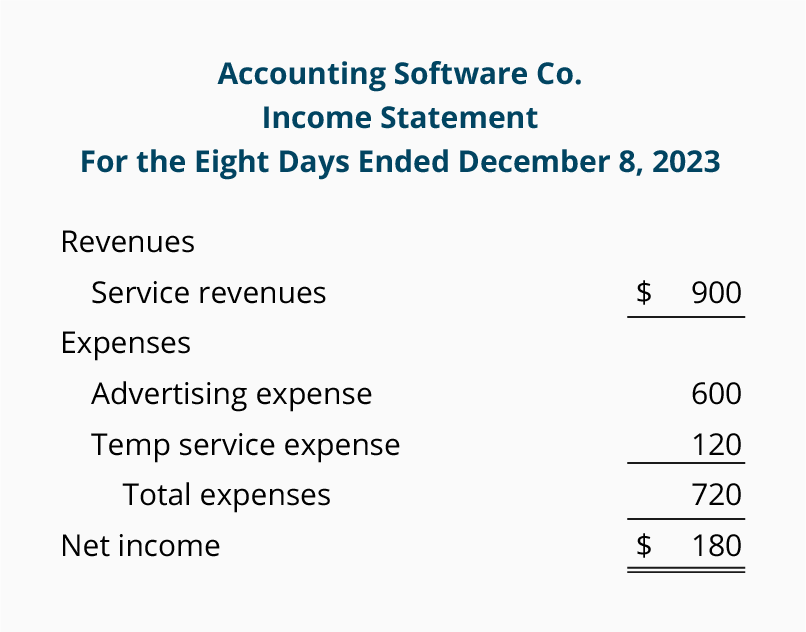

income statement for ASC for the eight days ending on December 8 is shown here:

Calculating a Missing Amount within Owner's Equity

The income statement for

the calendar year 2014 will explain a portion of the change in the owner's

equity between the balance sheets of December 31, 2013 and December 31, 2014.

The other items that account for the change in owner's equity are the owner's

investments into the sole proprietorship and the owner's draws (or

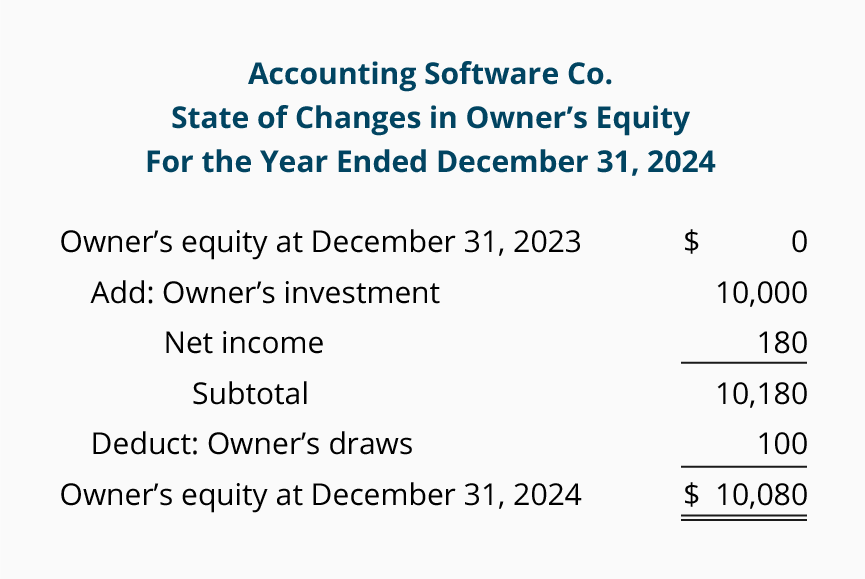

withdrawals). A recap of these changes is thestatement

of changes in owner's equity. Here is a statement of

changes in owner's equity for the year 2014 assuming that the Accounting

Software Co. had only the eight transactions that we covered earlier.

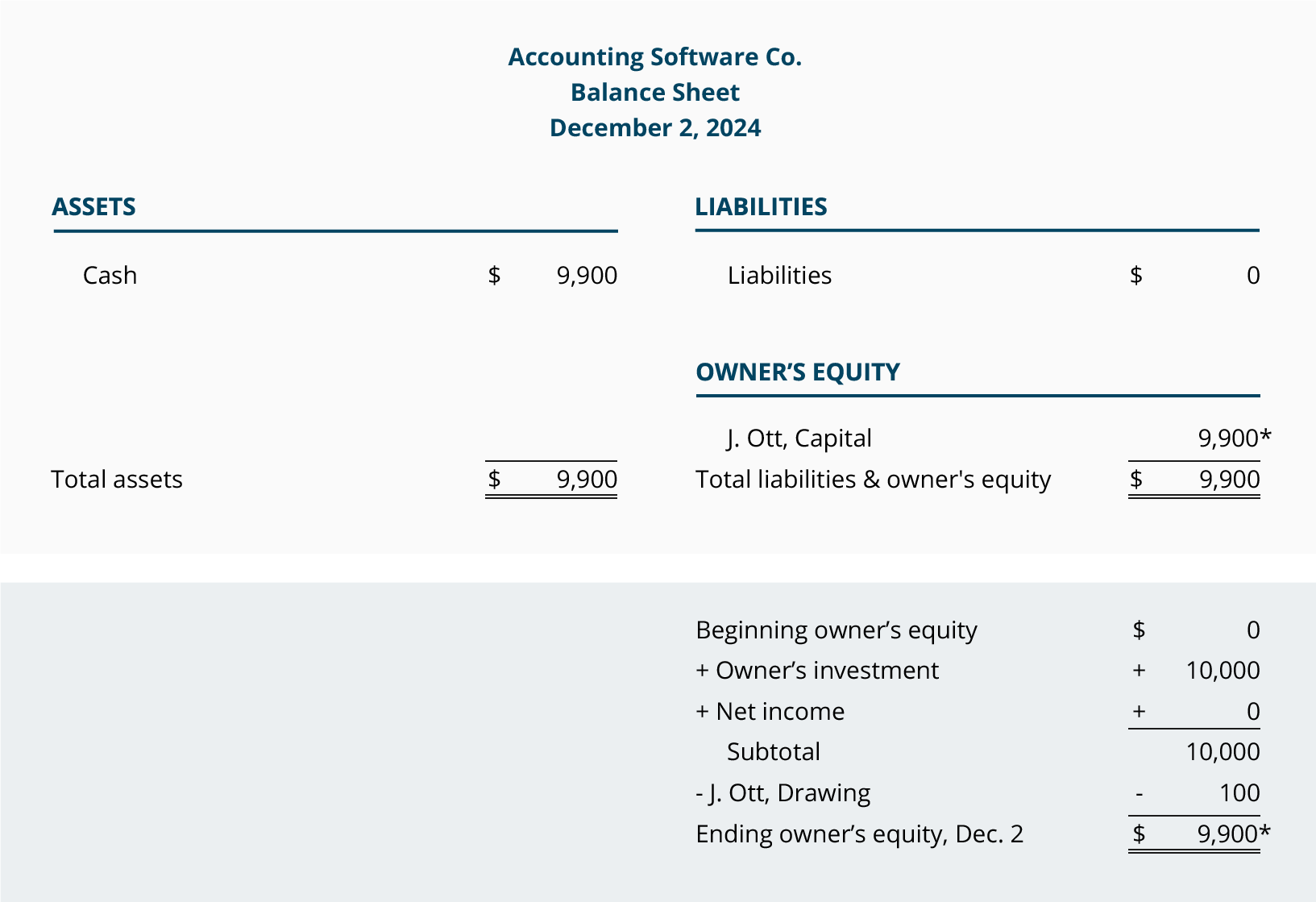

Example

of Calculating a Missing Amount

The

format of the statement of changes in owner's equity can be used to determine

one of these components if it is unknown. For example, if the net income for

the year 2014 is unknown, but you know the amount of the draws and the

beginning and ending balances of owner's equity, you can calculate the net

income. (This might be necessary if a company does not have complete records of

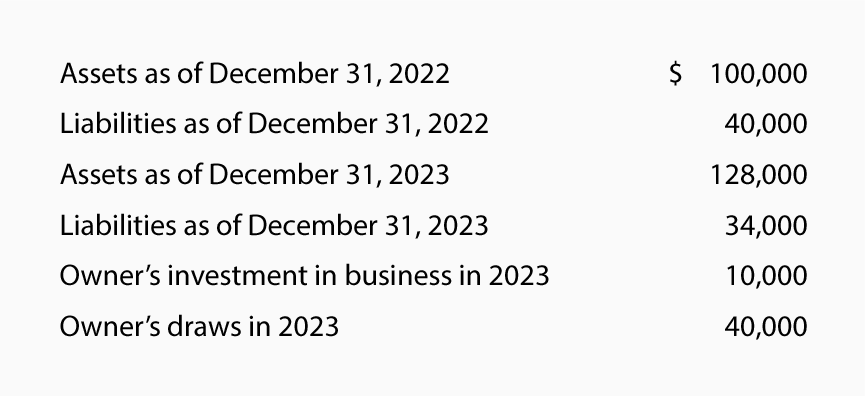

its revenues and expenses.) Let's demonstrate this by using the following

amounts.

Step

1.

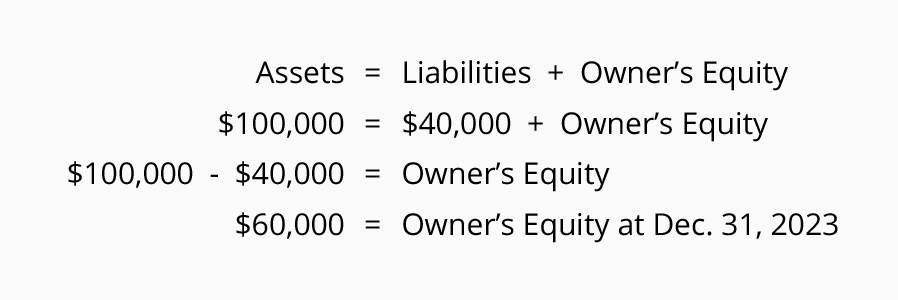

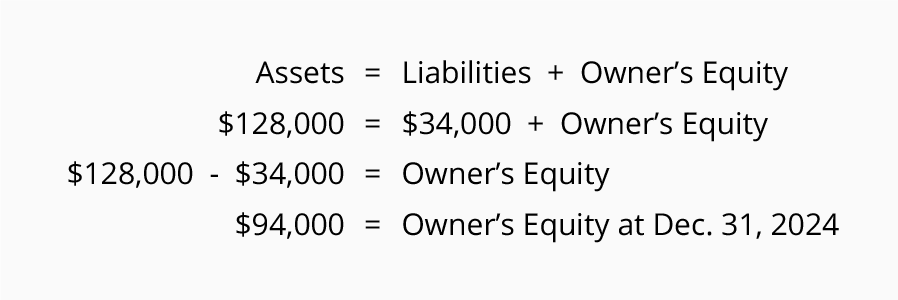

The owner's equity at December 31, 2013 can be computed using the accounting equation:

The owner's equity at December 31, 2013 can be computed using the accounting equation:

Step

2.

The owner's equity at December 31, 2014 can be computed as well:

The owner's equity at December 31, 2014 can be computed as well:

Step

3.

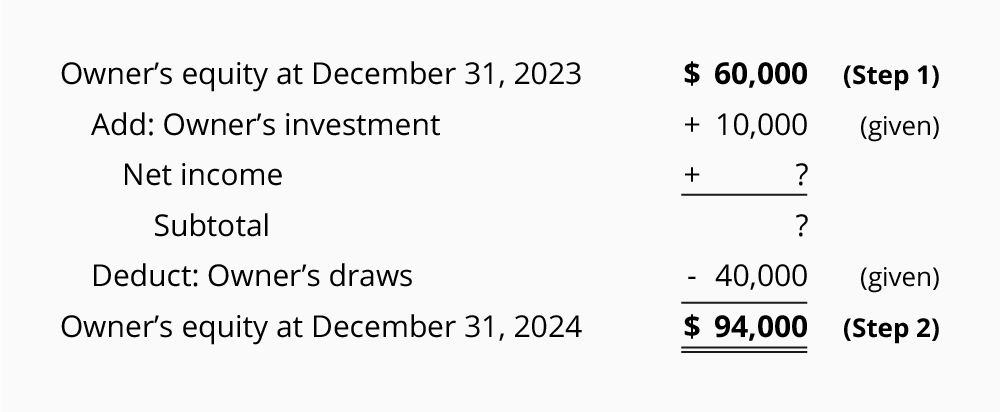

Insert into the statement of changes in owner's equity the information that was given and the amounts calculated in Step 1 and Step 2:

Insert into the statement of changes in owner's equity the information that was given and the amounts calculated in Step 1 and Step 2:

Step

4.

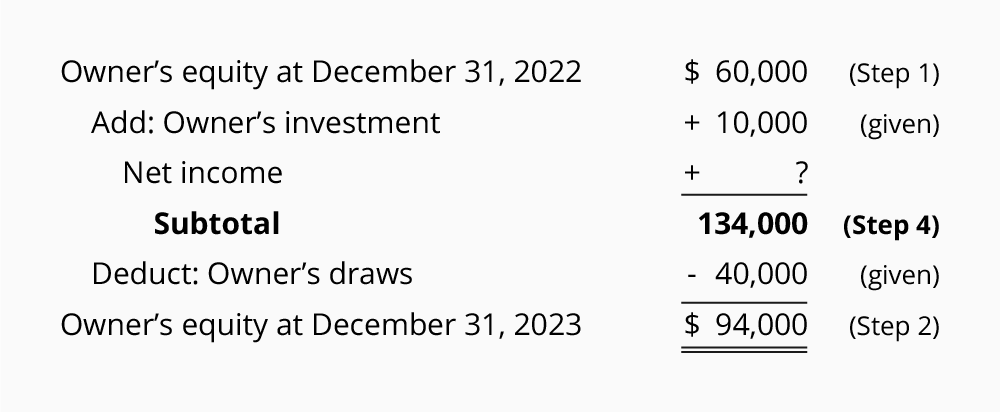

The "Subtotal" can be calculated by adding the last two numbers on the statement: $94,000 + $40,000 = $134,000. After this calculation we have:

The "Subtotal" can be calculated by adding the last two numbers on the statement: $94,000 + $40,000 = $134,000. After this calculation we have:

Step

5.

Starting at the top of the statement we know that the owner's equity before the start of 2014 was $60,000 and in 2014 the owner invested an additional $10,000. As a result we have $70,000 before considering the amount of Net Income. We also know that after the amount of Net Income is added, the Subtotal has to be $134,000 (the Subtotal calculated in Step 4). The Net Income is the difference between $70,000 and $134,000. Net income must have been $64,000.

Starting at the top of the statement we know that the owner's equity before the start of 2014 was $60,000 and in 2014 the owner invested an additional $10,000. As a result we have $70,000 before considering the amount of Net Income. We also know that after the amount of Net Income is added, the Subtotal has to be $134,000 (the Subtotal calculated in Step 4). The Net Income is the difference between $70,000 and $134,000. Net income must have been $64,000.

Step

6.

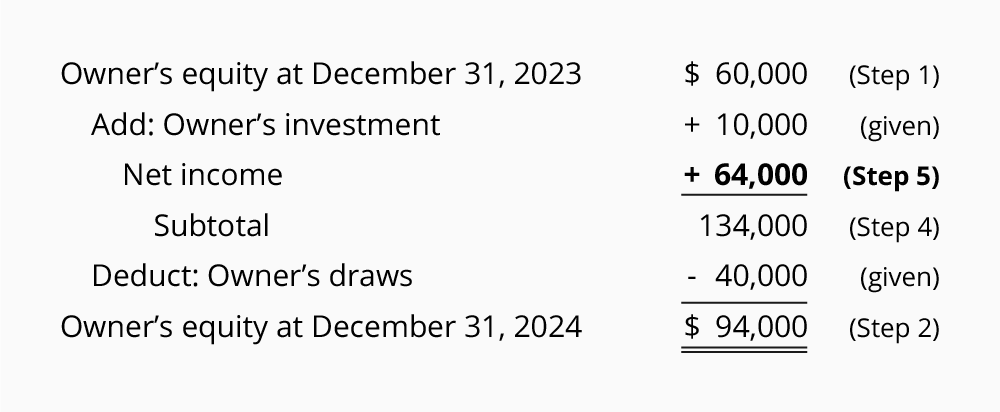

Insert the previously missing amount (in this case it is the $64,000 of net income) into the statement of changes in owner's equity and recheck the math:

Insert the previously missing amount (in this case it is the $64,000 of net income) into the statement of changes in owner's equity and recheck the math:

Since

the statement is mathematically correct, we are confident that the net income

was $64,000.

You can reinforce what you

have learned by using our Quiz for the Accounting Equation and our Crossword Puzzle on the Accounting Equation.

The

remaining parts of this topic will illustrate similar transactions and their

effect on the accounting equation when the company is a corporation instead of

a sole proprietorship.

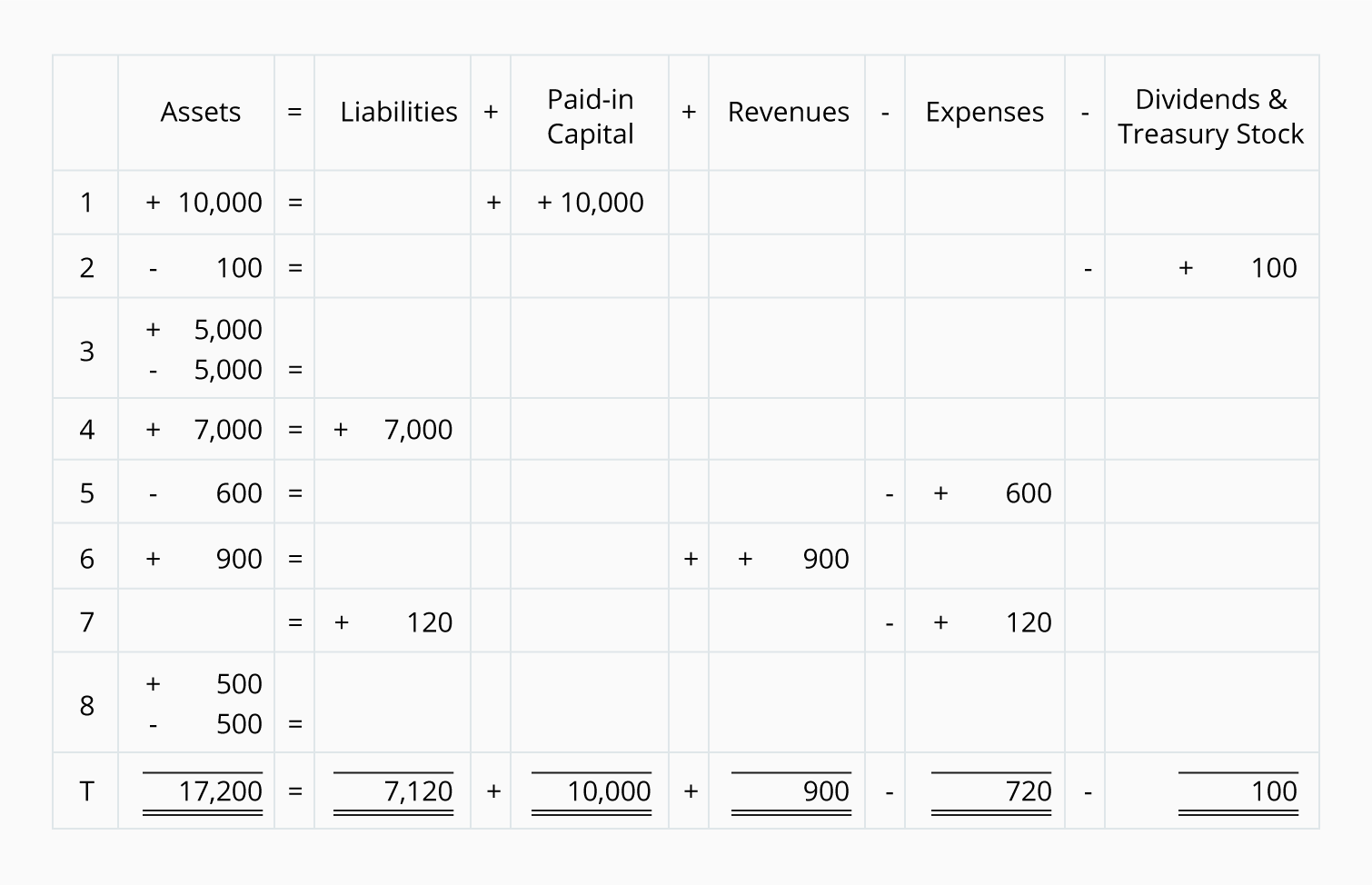

Accounting Equation for a Corporation: Transactions C1–C2

The

accounting equation (or basic accounting equation) for a corporation is

In

our examples below, we show how a given transaction affects the accounting

equation for a corporation. We also show how the same transaction will be

recorded in the company's general ledger accounts.

Our examples will also show

the effect of each transaction on the balance sheet and income statement. For

all of our examples we assume that the accrual basis of

accounting is being followed.

In

the examples that follow, we will use the following accounts:

- Cash

- Accounts Receivable

- Equipment

- Notes Payable

- Accounts Payable

- Common Stock

- Retained Earnings

- Treasury Stock

- Service Revenues

- Advertising Expense

- Temp Service Expense

(To view a more complete

listing of accounts for recording transactions, see the Explanation of Chart of Accounts.)

We

also assume that the corporation is a Subchapter S corporation in order to

avoid the income tax accounting that would occur with a "C"

corporation. (In a Subchapter S corporation the owners are responsible for the

income taxes instead of the corporation.)

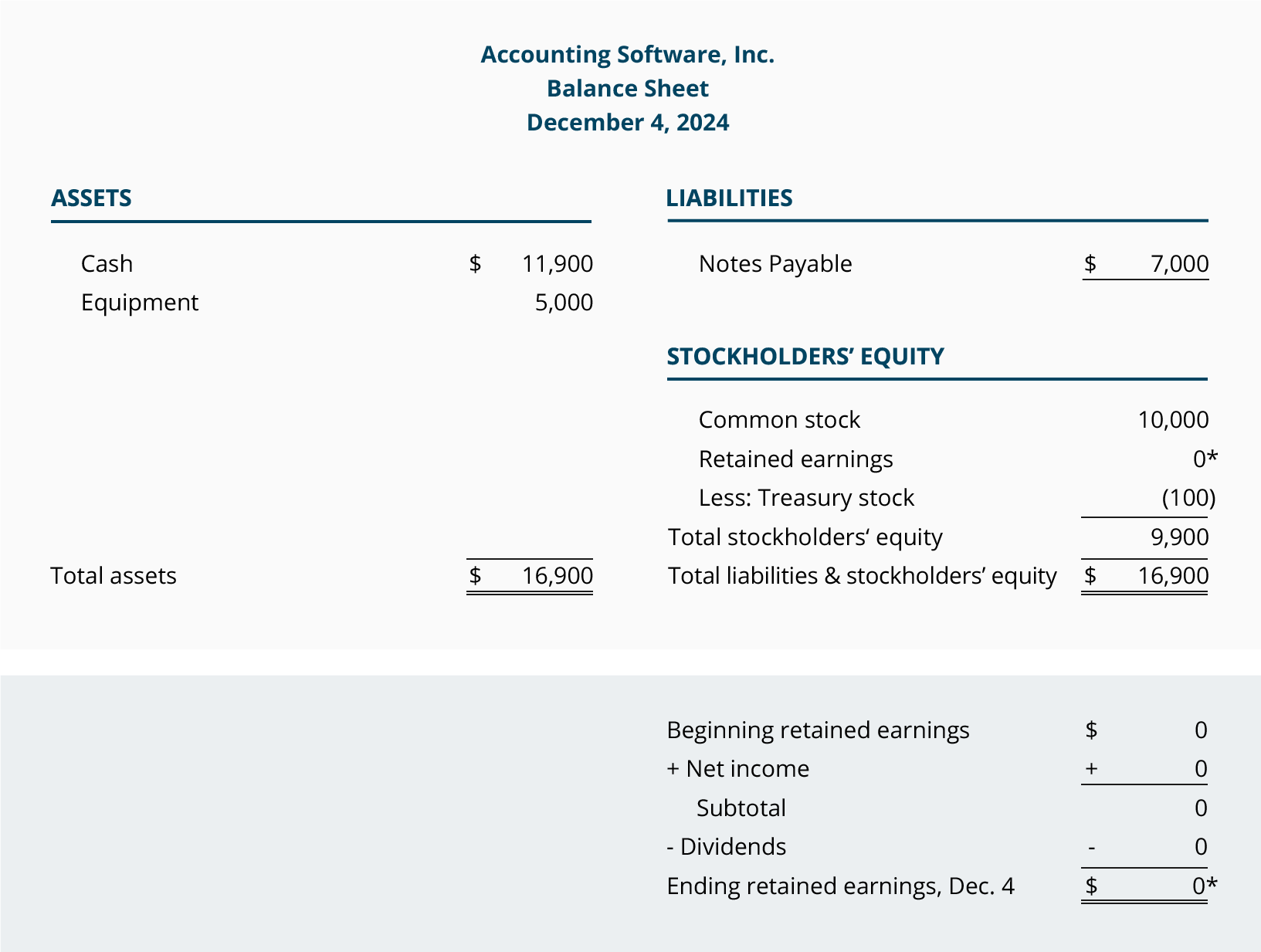

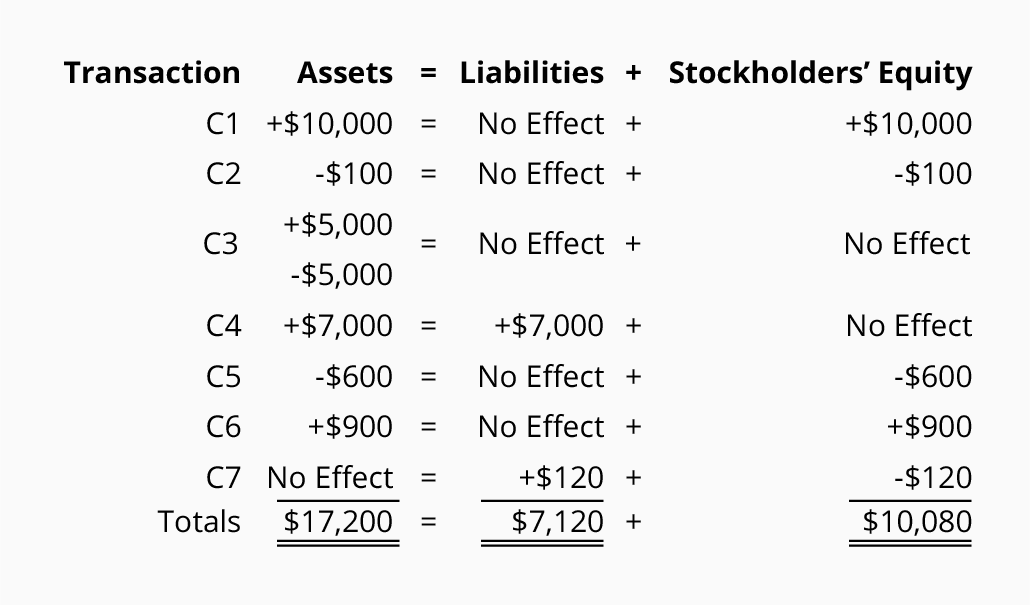

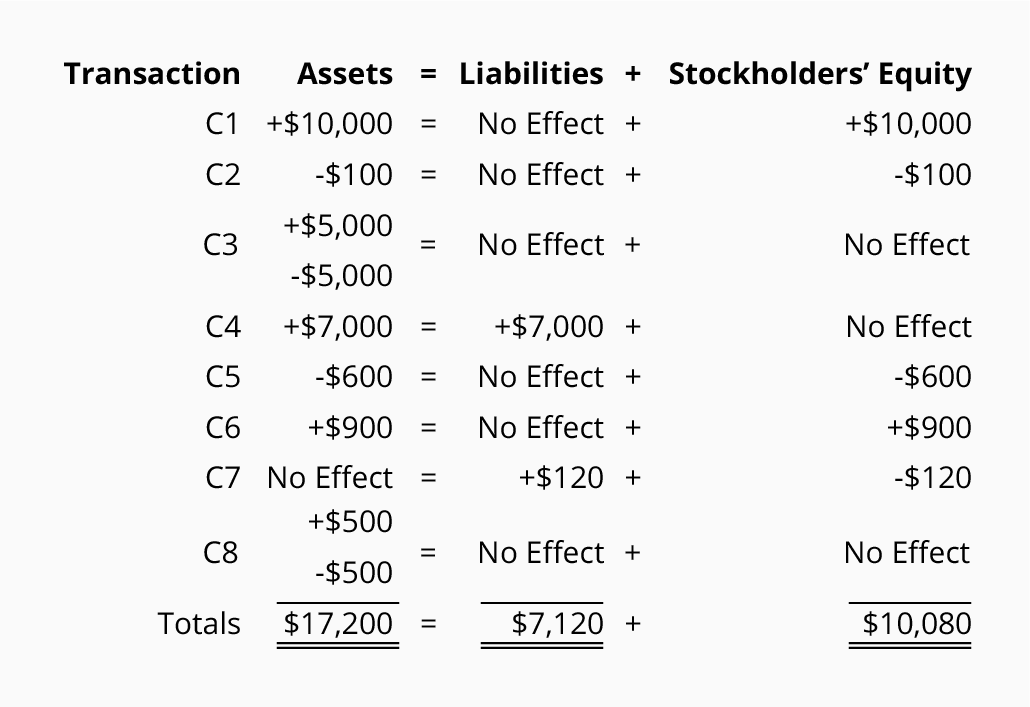

Corporation

Transaction C1

Let's

assume that members of the Ott family form a corporation called Accounting

Software, Inc. (ASI). On December 1, 2014, several members of the Ott family

invest a total of $10,000 to start ASI. In exchange, the corporation issues a

total of 1,000 shares of common stock. (The stock has no par value and no

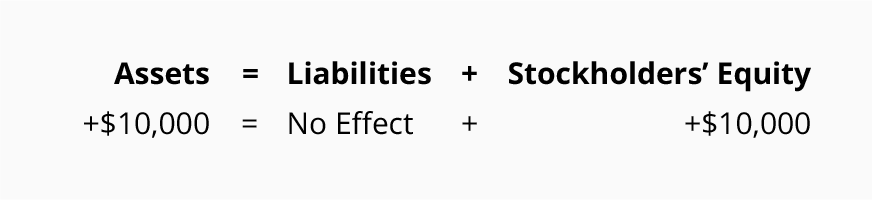

stated value.) The effect on the corporation's accounting equation is:

As

you see, ASI's assets increase by $10,000 and stockholders' equity increases by

the same amount. As a result, the accounting equation will be in balance.

The

accounting equation tells us that ASI has assets of $10,000 and the source of

those assets was the stockholders. Alternatively, the accounting equation tells

us that the corporation has assets of $10,000 and the only claim to the assets

is from the stockholders (owners).

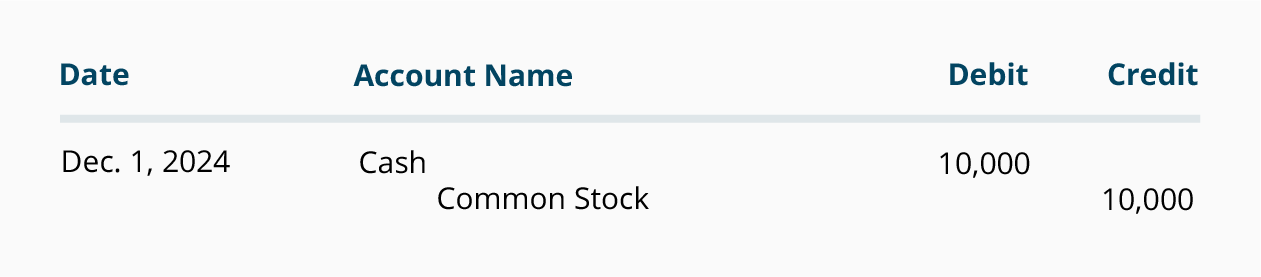

This

transaction is recorded in the asset account Cash and in the stockholders'

equity account Common Stock. The general journal entry to record the

transaction is:

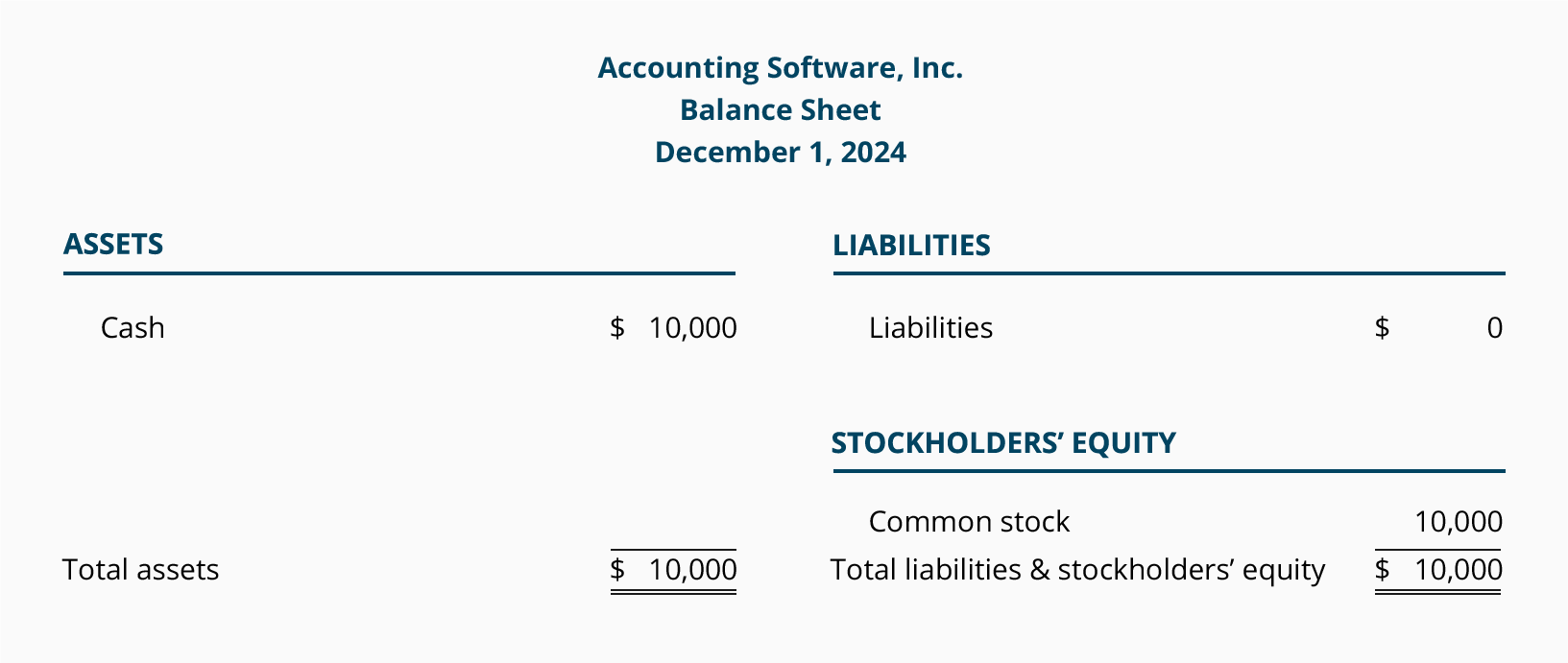

After

the journal entry is recorded in the accounts, a balance sheet can be prepared

to show ASI's financial position at the end of December 1, 2014:

The

purpose of an income statement is to report revenues and expenses. Since ASI

has not yet earned any revenues nor incurred any expenses, there are no

transactions to be reported on an income statement.

Corporation

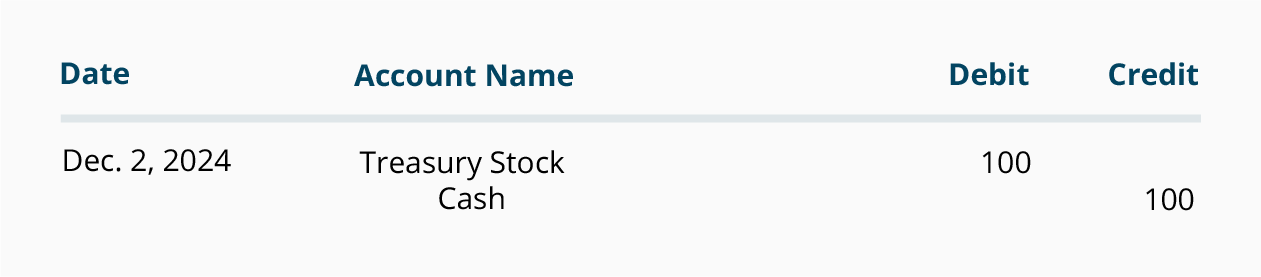

Transaction C2.

On December 2, 2014 ASI

purchases $100 of its stock from one of its stockholders. The stock will be

held by the corporation as Treasury Stock.

The effect of the accounting equation is:

The

purchase of its own stock for cash meant that ASI's assets decrease by $100 and

its stockholders' equity decreases by $100.

This

transaction is recorded in the asset account Cash and in the stockholders'

equity account Treasury Stock. The accounting entry in general journal form is:

Since

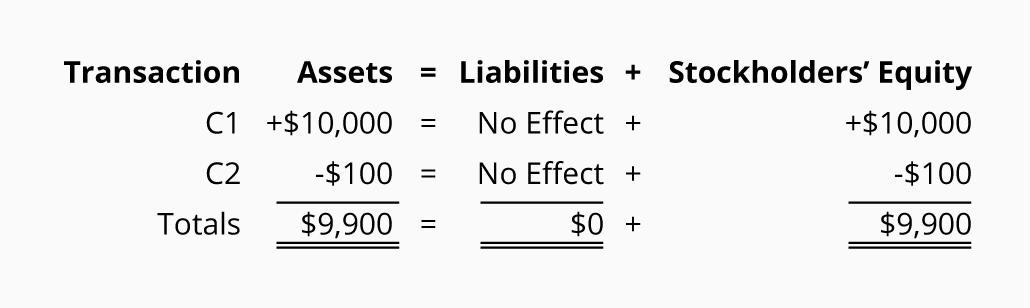

the transactions of December 1 and 2 were each in balance, the sum of both

transactions should also be in balance:

The

totals indicate that ASI has assets of $9,900 and the source of those assets is

the stockholders. The accounting equation also shows that the corporation has

assets of $9,900 and the only claim against those resources is the

stockholders' claim.

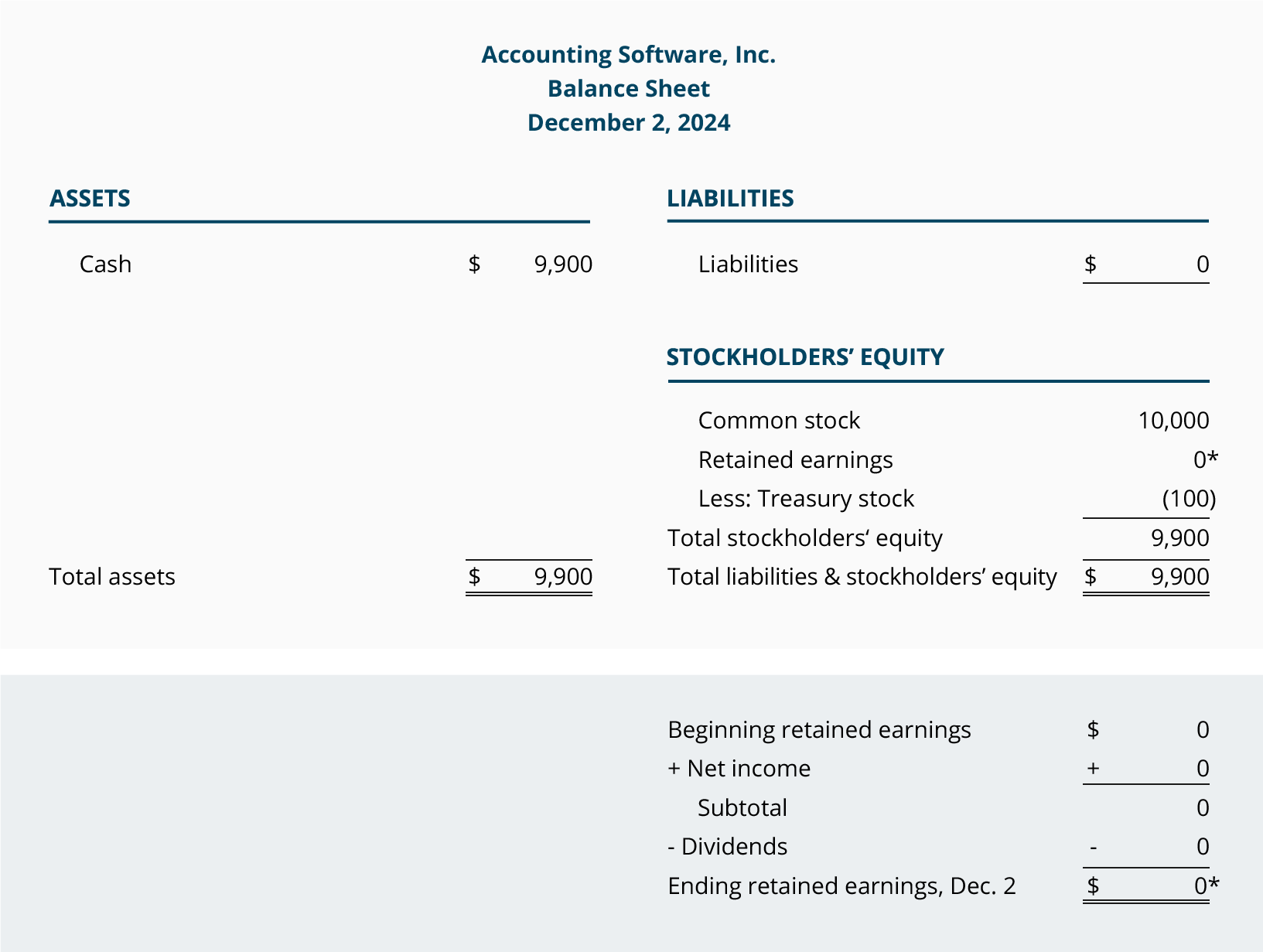

The

December 2 balance sheet will communicate the corporation's financial position

as of midnight on December 2:

The

purchase of a corporation's own stock will never result in an amount to be

reported on the income statement.

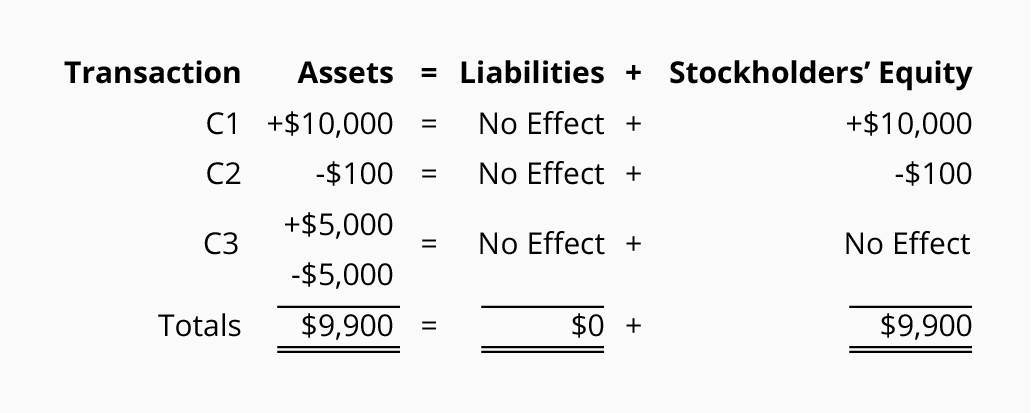

Accounting Equation for a Corporation: Transactions C3–C4

Corporation

Transaction C3.

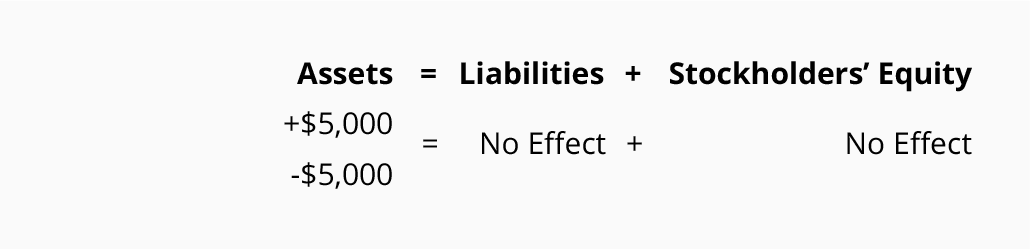

On

December 3, 2014 ASI spends $5,000 of cash to purchase computer equipment for

use in the business. The effect of this transaction on its accounting equation

is:

The

accounting equation indicates that one asset increases and one asset decreases.

Since the amount of the increase is the same as the amount of the decrease, the

accounting equation remains in balance.

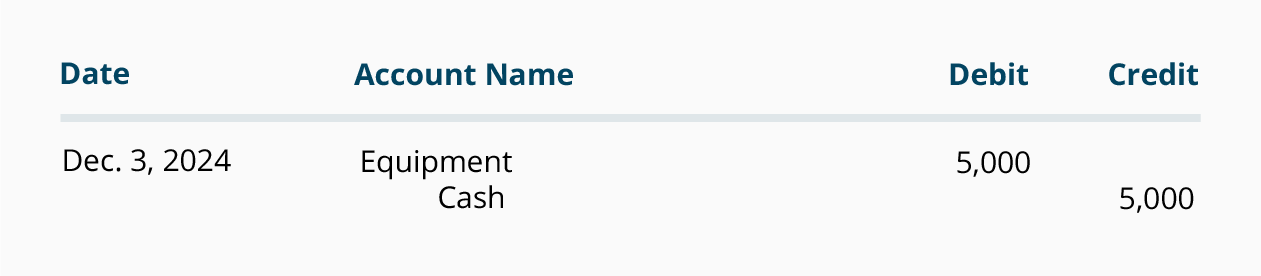

This

transaction is recorded in the asset accounts Equipment and Cash. The account

increases by $5,000 and the account decreases by $5,000. The journal entry for

this transaction is:

The

effect on the accounting equation from the first three transactions is:

The

totals tell us that the corporation has assets of $9,900 and the source of

those assets is the stockholders. The totals tell us that the company has

assets of $9,900 and that the only claim against those assets is the

stockholders' claim.

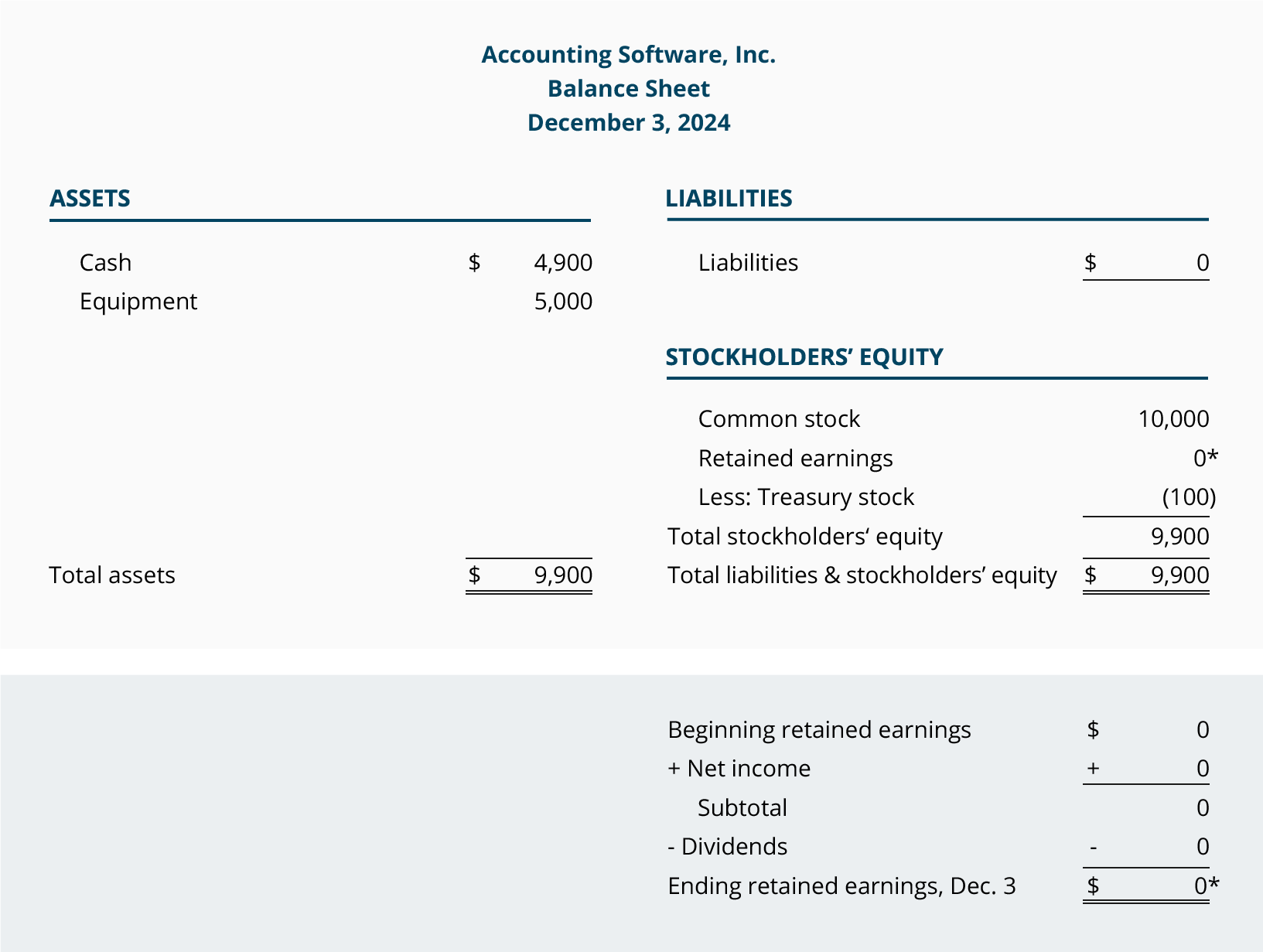

The

balance sheet dated December 3, 2014 reflects the financial position of the

corporation as of midnight on December 3:

The purchase of equipment

is not an immediate expense. It will become depreciation expenseonly

after the equipment is placed in service. We will assume that as of December 3

the equipment has not been placed into service. Therefore, there is no expense

in this transaction or in the earlier transactions to be reported on the income

statement.

Corporation

Transaction C4.

On

December 4, 2014 ASI obtains $7,000 by borrowing money from its bank. The

effect of this transaction on the accounting equation is:

As

you see, ACI's assets increase and its liabilities increase by $7,000.

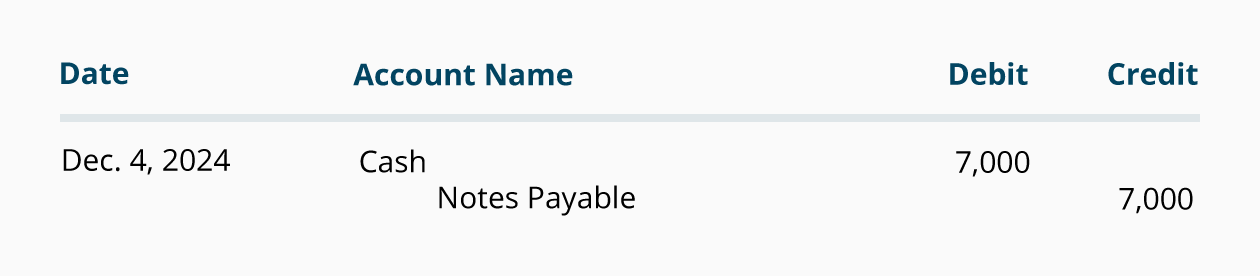

This

transaction is recorded in the asset account Cash and the liability account

Notes Payable with the following journal entry:

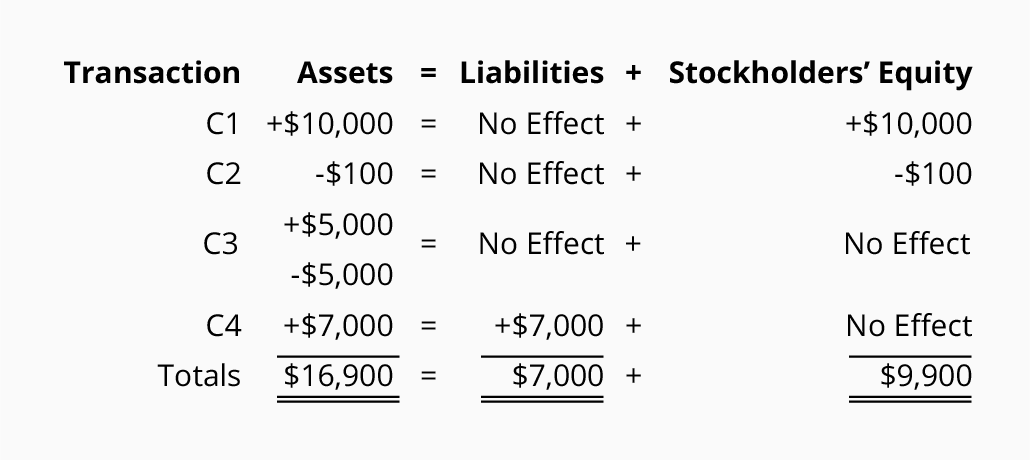

To

see the effect on the accounting equation from the first four transactions,

click here:

These

totals indicate that the transactions through December 4 result in assets of

$16,900. There are two sources for those assets: the creditors provided $7,000

of assets, and the stockholders provided $9,900. You can also interpret the

accounting equation to say that the corporation has assets of $16,900 and the

creditors have a claim of $7,000. The residual or remainder of $9,900 is the

stockholders' claim.

The

balance sheet dated December 4 reports the corporation's financial position as

of that date:

The

receipt of money from the bank loan is not revenue since ASI did not earn the

money by providing services, investing, etc. As a result, there is no income

statement effect from this transaction or earlier transactions.

Accounting Equation for a Corporation: Transactions C5–C6

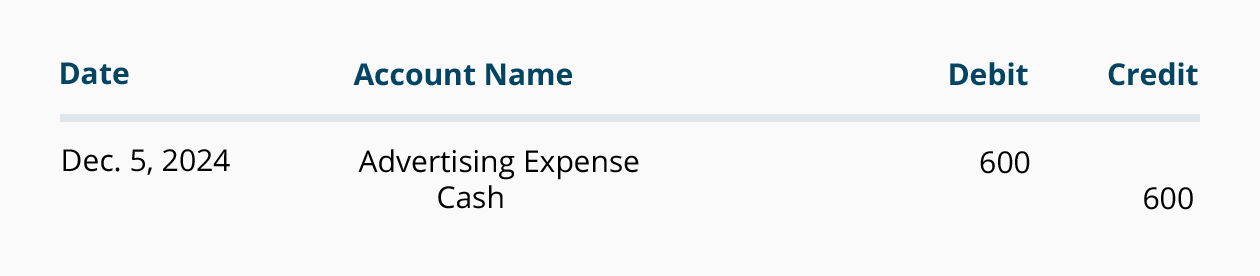

Corporation

Transaction C5.

On

December 5, 2014 Accounting Software, Inc. pays $600 for ads that were run in

recent days. The effect of the advertising transaction on the corporation's

accounting equation is:

Since ASI is

paying $600,

its assets decrease. The second effect is a $600 decrease in stockholders'

equity, because the transaction involves an expense. (An expense is a cost that

is used up or its future economic value cannot be measured.)

Although

stockholders' equity decreases because of an expense, the transaction is not

recorded directly into the retained earnings account. Instead, the amount is

initially recorded in the expense account Advertising Expense and in the asset

account Cash. The journal entry for this transaction is:

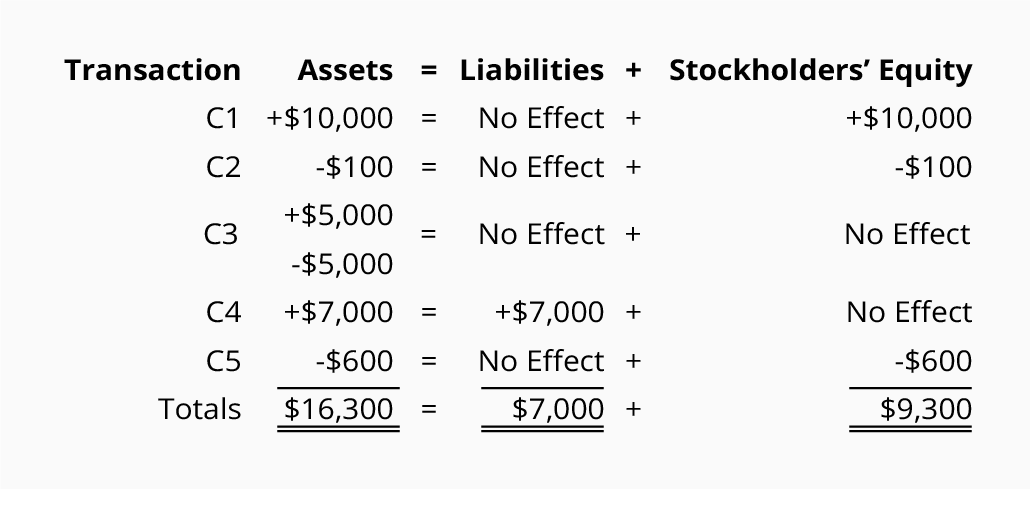

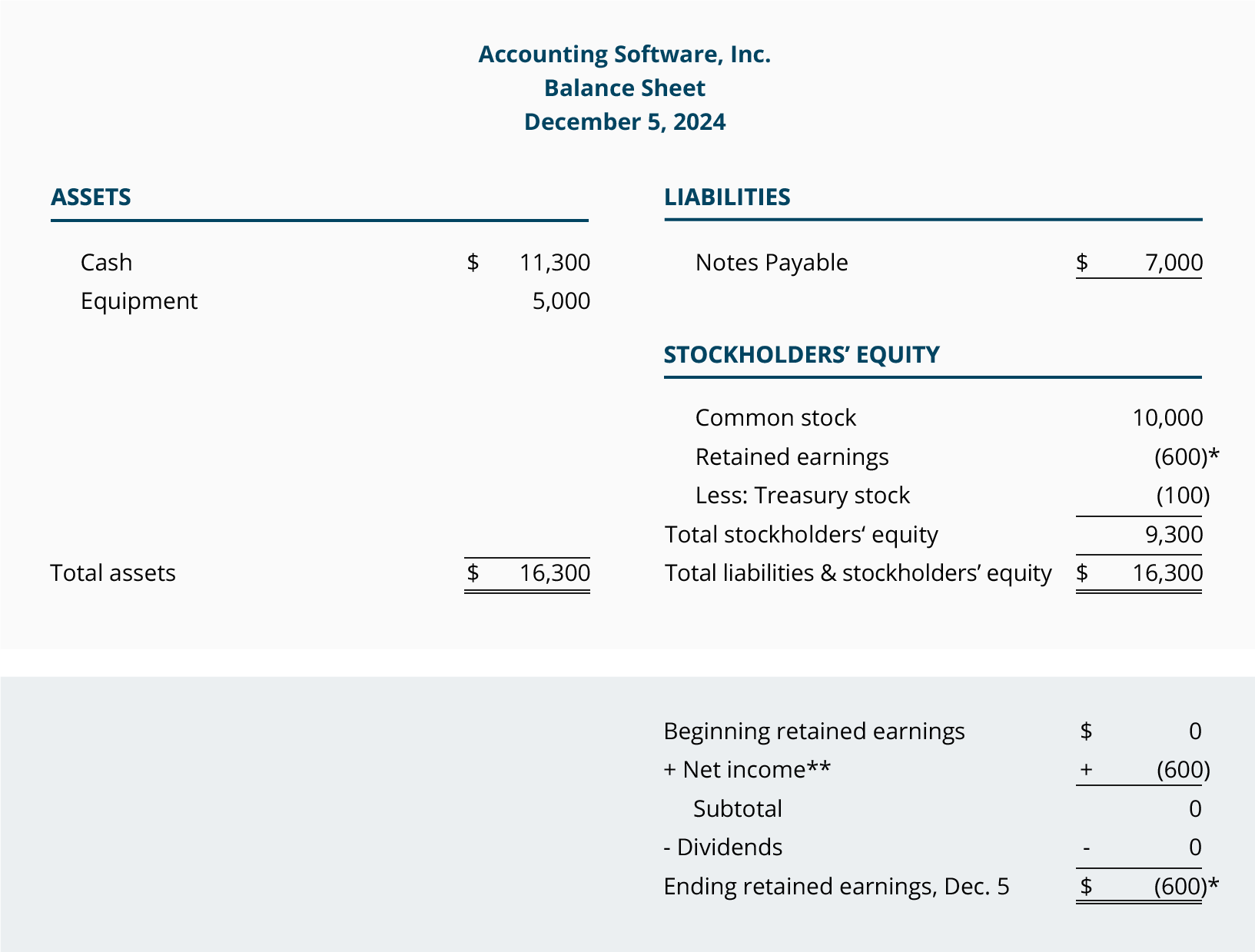

The

combined effect of the first five transactions is:

The

totals now indicate that Accounting Software, Inc. has assets of $16,300. The

creditors provided $7,000 and the stockholders provided $9,300. Viewed another

way, the corporation has assets of $16,300 with the creditors having a claim of

$7,000 and the stockholders having a claim of $9,300.

The

balance sheet as of the end of December 5, 2014 is presented here:

**The

income statement (which reports the company's revenues, expenses, gains, and

losses for a specified time period) is a link between balance sheets. It

provides the results of operations—an important part of the change in retained

earnings and stockholders' equity.

Since

this transaction involves an expense, it will affect ASI's income statement.

The corporation's income statement for the first five days of December is

presented here:

Because

we assume that Accounting Services, Inc. is a Subchapter S corporation, income

tax expense is not reported on the corporation's income statement.

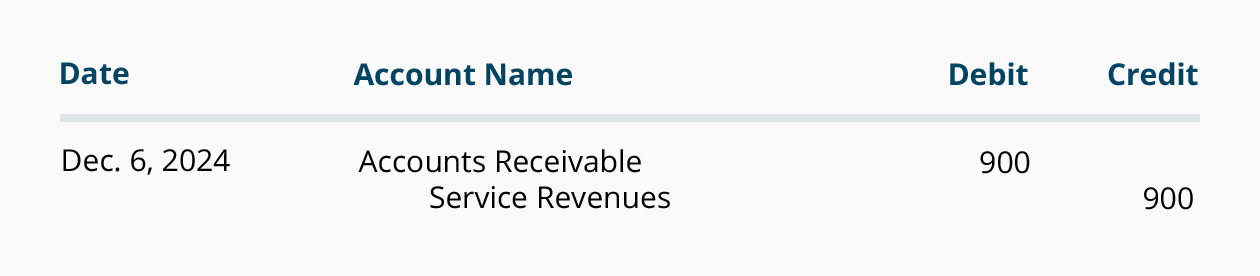

Corporation

Transaction C6.

On

December 6, 2014 ASI performs consulting services for its clients. The clients

are billed for the agreed upon amount of $900. The amounts are due in 30 days.

The effect on the accounting equation is:

Since ASI has performed the

services, it has earned revenues and it has the right to

receive $900 from its clients. This right means that assets increased. The

earning of revenues also causes stockholders' equity to increase.

Although revenues cause

stockholders' equity to increase, the revenue transaction is not recorded

directly into a stockholders' equity account at this time. Rather, the amount

earned is recorded in the revenues account Service Revenues . This will allow the corporation to

report the revenues account on its income statement at any time. (After the

year ends, the amount in the revenues accounts will be transferred to the

retained earnings account.) The general journal entry for providing services on

credit is:

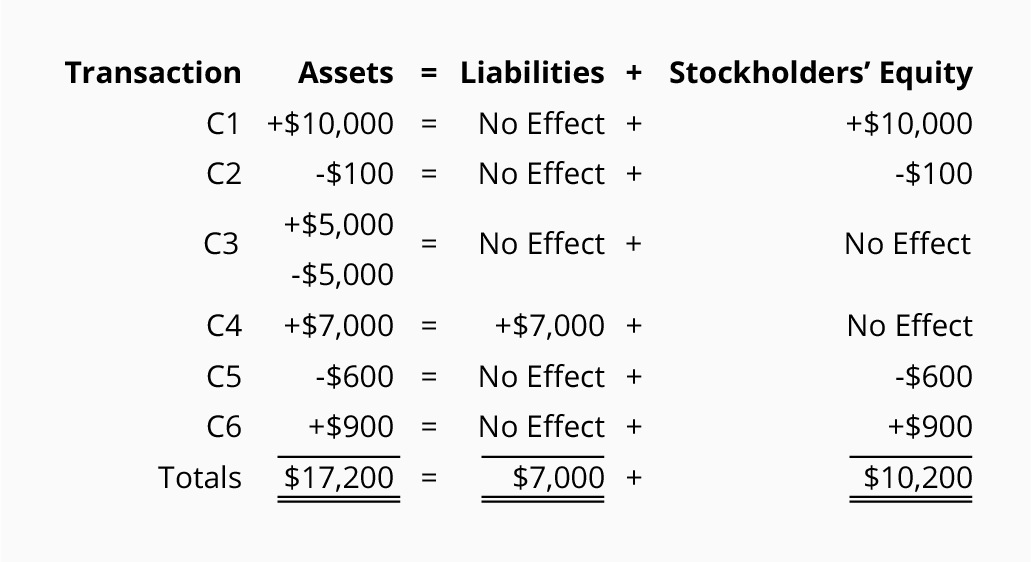

The

effect on the accounting equation from the first six transactions can be viewed

here:

The

totals tell us that at the end of December 6, the corporation has assets of

$17,200. It also shows that $7,000 of the assets came from creditors and that

$10,200 came from stockholders. The totals can also be viewed another way: ASI

has assets of $17,200 with its creditors having a claim of $7,000 and the

stockholders having a claim for the remainder or residual of $10,200.

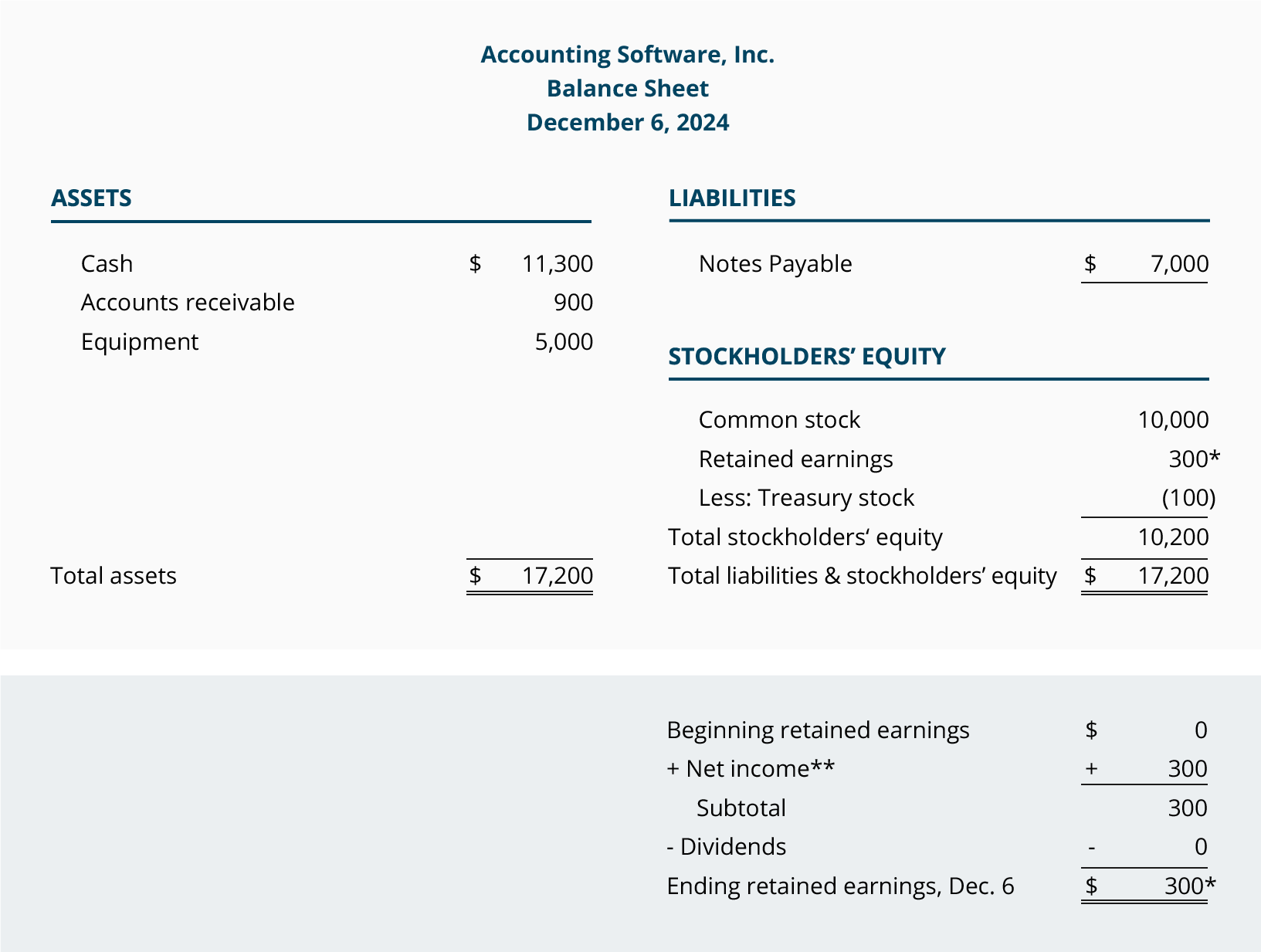

The